Fee-Only Advice: Protecting Your Interests Abroad

- Jan 12

- 7 min read

Fee-only advice has become the preferred choice for over half of American expatriates moving to France, Portugal, or Spain each year. Managing cross-border taxes, retirement accounts, and investments can feel even more complicated when you factor in British financial systems and local regulations. This guide explains how fee-only advisers offer true transparency, helping you avoid conflicts of interest and protect your financial future as you settle into European life.

Table of Contents

Key Takeaways

Point | Details |

Fee-Only Advice Prioritises Client Interests | Fee-only advisers are compensated directly by clients, ensuring unbiased advice that aligns with financial wellness. |

Transparency in Pricing Models | Various fee structures, such as hourly rates and retainers, provide clients with clear insights into advisory costs. |

Importance of Regulatory Standards | Adhering to stringent regulatory guidelines protects investors and ensures advisers act in their clients’ best interests. |

Benefits for American Expatriates | Fee-only advisers help expats navigate complex financial landscapes with tailored, conflict-free strategies. |

What Fee-Only Advice Means Explained

Fee-only financial advice represents a transparent approach to financial planning where advisers are compensated directly by their clients, eliminating potential conflicts of interest. Unlike commission-based models, these professionals charge predetermined fees for their services without earning additional income from product sales or recommendations. Independent financial advisers prioritise client interests above all other considerations.

The National Association of Personal Financial Advisors (NAPFA) establishes critical standards for fee-only advisers, ensuring they maintain strict ethical guidelines. These professionals typically charge through several transparent methods: hourly rates, percentage of assets managed, fixed retainer fees, or project-based pricing. By removing product commissions, fee-only advisers create a direct alignment between their recommendations and clients’ financial wellness.

For American expatriates navigating complex international financial landscapes, fee-only advice offers several significant advantages. These include unbiased investment recommendations, clear cost structures, and personalised strategies tailored to individual financial goals. Advisers receive compensation solely from client fees, which means their advice is not influenced by potential sales incentives or hidden financial motivations.

Pro Tip: Always request a comprehensive fee disclosure document and confirm the exact compensation structure before engaging with any financial adviser to understand precisely how and what you will be charged.

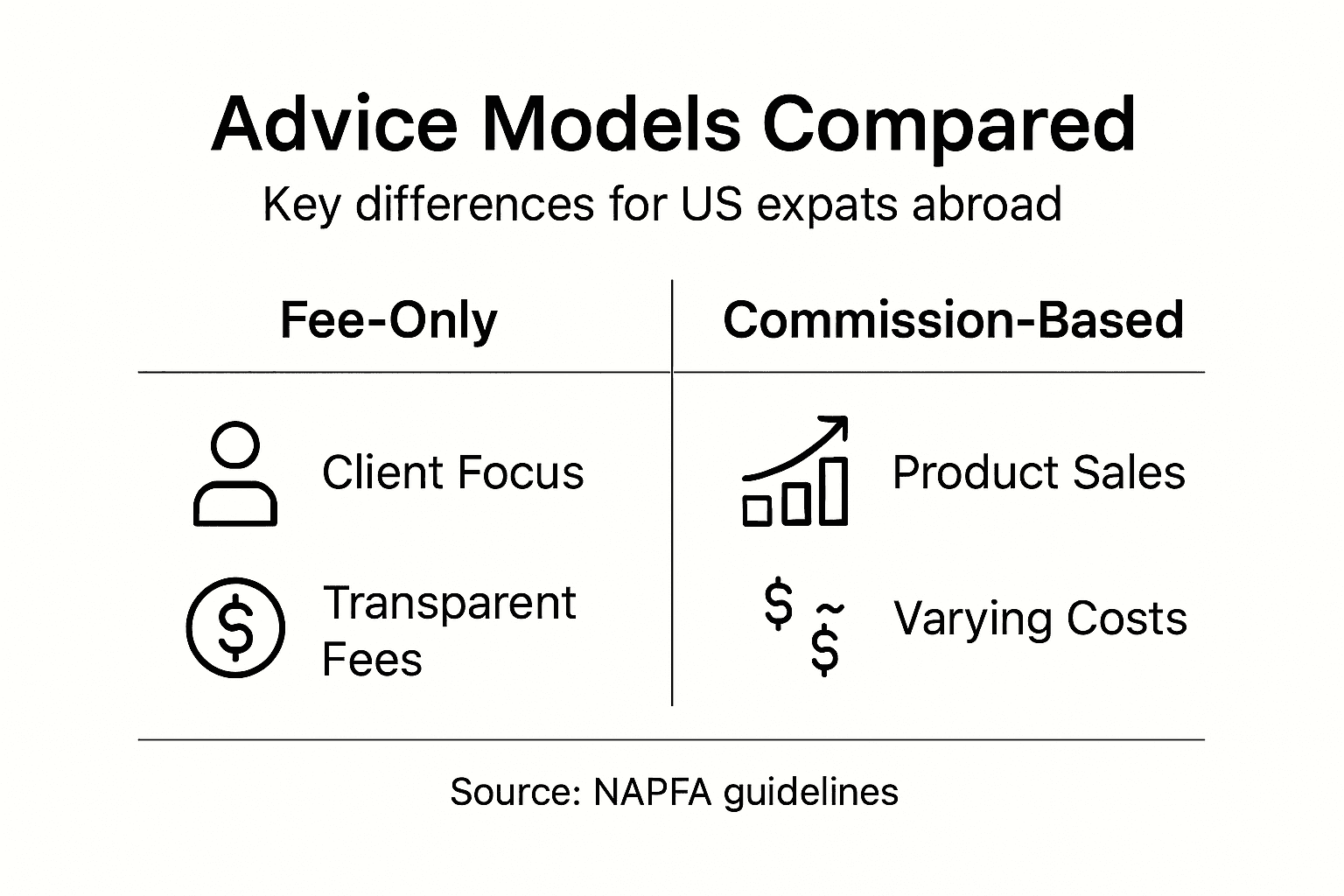

Key Differences With Commission-Based Advice

Commission-based financial advice fundamentally differs from fee-only models through its compensation structure. Financial advisor compensation methods create inherent conflicts of interest where advisers earn money through product sales rather than direct client fees. This means recommendations might prioritise financial products generating higher commissions over client’s optimal financial outcomes.

Under commission-based models, advisers typically earn percentages from selling financial products like mutual funds, insurance policies, or investment vehicles. Commission-based advice structures inherently incentivise recommending specific products that generate more substantial income, potentially compromising objective financial guidance. Unlike fee-only advisers who charge transparent, predetermined fees, commission-based professionals embed their compensation within product pricing.

The key distinctions become particularly critical for American expatriates managing complex international financial portfolios. Commission-based advisers may push products offering higher commissions, whereas fee-only professionals provide recommendations solely based on client interests. This fundamental difference ensures fee-only advisers maintain fiduciary responsibilities without external financial motivations influencing their strategic counsel.

Here is a side-by-side comparison of fee-only and commission-based financial advice approaches:

Criteria | Fee-Only Advice | Commission-Based Advice |

Compensation Source | Direct client fees | Product sales commissions |

Potential Conflicts | Minimal | Higher due to sales incentives |

Typical Pricing Models | Hourly, retainer, assets | Percentage of product sold |

Recommendation Bias | Client interests prioritised | Product-driven recommendations |

Pro Tip: Request a comprehensive breakdown of all potential fees and commissions before engaging any financial adviser to understand precisely how their recommendations might be financially influenced.

Legal Standards And Regulatory Oversight

Financial regulatory bodies play a critical role in ensuring the integrity and transparency of financial advisory services across international markets. Financial Stability Board standards establish comprehensive guidelines that protect investors by mandating rigorous oversight of financial advisers’ professional conduct. These international frameworks focus on creating robust mechanisms to minimise conflicts of interest and maintain the highest levels of professional accountability.

For American expatriates seeking financial advice abroad, understanding regulatory protections becomes paramount. Investment adviser regulations mandate comprehensive disclosure requirements, ensuring that advisers provide transparent information about fees, potential conflicts, and their fiduciary responsibilities. The Securities and Exchange Commission enforces strict guidelines that require advisers to act exclusively in their clients’ best interests, with particular emphasis on clear fee structures and comprehensive financial reporting.

International regulatory frameworks increasingly recognise the complexity of cross-border financial management. Different jurisdictions maintain unique oversight mechanisms, but core principles remain consistent: protecting investor interests, ensuring transparent fee disclosures, and maintaining the highest standards of professional ethics. American expatriates must carefully verify an adviser’s regulatory credentials, confirming their compliance with both local and international financial standards.

Pro Tip: Always request a detailed compliance certificate and verify an adviser’s regulatory registrations across relevant jurisdictions before engaging their services.

Benefits For US Expats In Europe

American expatriates in Europe face unique financial challenges that require specialised guidance, making fee-only advice critical for navigating complex international financial landscapes. These advisers provide transparent, unbiased recommendations tailored specifically to the intricate cross-border financial requirements of US citizens living abroad, addressing everything from taxation complexities to retirement planning strategies.

Retirement and investment solutions for expatriates offer significant advantages through fee-only financial advice. These professionals help US expats develop personalised financial strategies that account for unique international residency challenges, such as managing retirement accounts across different jurisdictions, understanding tax implications, and selecting investment vehicles compatible with both US and European financial regulations.

The primary benefits include comprehensive, conflict-free financial guidance that prioritises the expatriate’s long-term financial wellness. Fee-only advisers provide detailed insights into international investment opportunities, tax-efficient retirement planning, and strategic wealth management that considers the complex legal and financial environments of multiple countries. Their approach ensures that recommendations are driven solely by the client’s best interests, rather than potential product commissions.

Pro Tip: Request a comprehensive global financial review that specifically addresses your cross-border financial challenges before finalising any international investment strategies.

Comparing Costs And Potential Pitfalls

Understanding the nuanced cost structures of financial advice is crucial for American expatriates seeking professional guidance. Fee billing practices in financial advisory services reveal multiple potential charging models, ranging from flat fees and hourly rates to percentage-based asset management charges. These transparent pricing mechanisms differ substantially from traditional commission-based approaches, offering clients clearer insights into their actual advisory expenses.

Financial advisor compensation structures demonstrate significant variations that can impact overall investment strategies. Fee-only advisers typically charge upfront or ongoing fees irrespective of investment performance, which ensures their recommendations remain unbiased. In contrast, commission-based models embed costs within product sales, potentially creating hidden financial incentives that might compromise objective advice.

This summary highlights common charging methods for financial advisers and their impact on transparency:

Charging Method | Description | Transparency | Typical Use Cases |

Hourly Rate | Fee per hour of service | High | One-off consultations |

Percentage of Assets | Fee based on assets managed | Moderate | Ongoing portfolio management |

Fixed Retainer | Regular flat fee | High | Comprehensive advisory |

Commission | Payment from products sold | Low | Insurance and investment sales |

Potential pitfalls for US expatriates include insufficient fee disclosure, unexpected additional charges, and complex international regulatory compliance requirements. Clients must carefully scrutinise advisory agreements, understanding precisely how fees are calculated, charged, and what services they encompass. This diligence helps prevent misunderstandings and ensures alignment between financial advice costs and expected professional services.

Pro Tip: Request a comprehensive, written fee breakdown that details all potential charges, including potential currency conversion costs and international transaction expenses, before finalising any financial advisory agreement.

Secure Your Financial Future Abroad With Trusted Fee-Only Advice

Navigating the complex world of cross-border finances as an American expatriate can feel overwhelming. The article highlights key challenges such as hidden fees, potential conflicts from commission-based advice, and the need for transparent, personalised financial guidance that prioritises your best interests. If you want to avoid biased recommendations and ensure your investments, taxes, and retirement plans are managed with clear fee structures and full compliance, relying on verified fee-only experts is essential.

At Linkindependent, we specialise in connecting US citizens living in Europe and beyond with licensed financial advisers who provide unbiased, fee-only advice tailored to your unique international needs. Whether you require comprehensive wealth planning, help with 401k pensions, or cross-border tax solutions our platform offers an easy three-step process to find trusted professionals regulated across multiple jurisdictions. Take control of your finances today with advisers dedicated to protecting your interests without hidden commissions or conflicts.

Discover how transparent fee-only financial advice can empower your financial decisions abroad. Start your journey now by visiting Linkindependent and get matched with expert advisers who truly prioritise your long-term financial wellbeing.

Frequently Asked Questions

What is fee-only financial advice?

Fee-only financial advice refers to a compensation model where financial advisers are paid directly by their clients. This model eliminates potential conflicts of interest associated with commission-based advice, as advisers do not earn additional income from product sales.

How does fee-only advice differ from commission-based advice?

Fee-only advice differs primarily in its compensation structure. Fee-only advisers charge predetermined fees for their services, while commission-based advisers earn money through the sale of financial products. This can lead to conflicts of interest where recommendations may favour products that generate higher commissions.

What are the benefits of fee-only advice for expats?

Fee-only advice benefits expatriates by providing unbiased investment recommendations tailored to their unique financial situations. This approach ensures that financial strategies consider international complexities, such as tax implications and retirement planning across different jurisdictions.

How can I ensure I’m not being charged hidden fees by my financial adviser?

To avoid hidden fees, always request a detailed fee disclosure document from your financial adviser. This document should outline all potential charges, including any additional costs related to services, currency conversions, or international transactions.

Recommended

Comments