Why Avoid Commission-Based Advice Abroad

- Feb 17

- 8 min read

Finding truly impartial guidance can feel like a challenge for American professionals setting up a new life in Europe. Hidden incentives built into commission-based advice often mean recommendations favour expensive products rather than your best interests. For anyone facing complex cross-border tax rules or charting an international investment plan, understanding the risks of commission arrangements is vital. This guide breaks down why commission-based financial advice creates powerful conflicts of interest and highlights alternative fee-only approaches that protect your wealth as an American in Europe.

Table of Contents

Key Takeaways

Point | Details |

Conflict of Interest in Commission-Based Advice | Commission-based financial advisers may prioritise their earnings over client welfare, potentially recommending less suitable investment products. |

Importance of Fee Structures | Understanding different fee structures, such as asset-based fees and hourly rates, is crucial for expatriates seeking unbiased financial advice. |

Cross-Border Financial Risks for Expatriates | American expatriates face unique financial challenges, including complex taxation and regulatory compliance, requiring specialised financial guidance. |

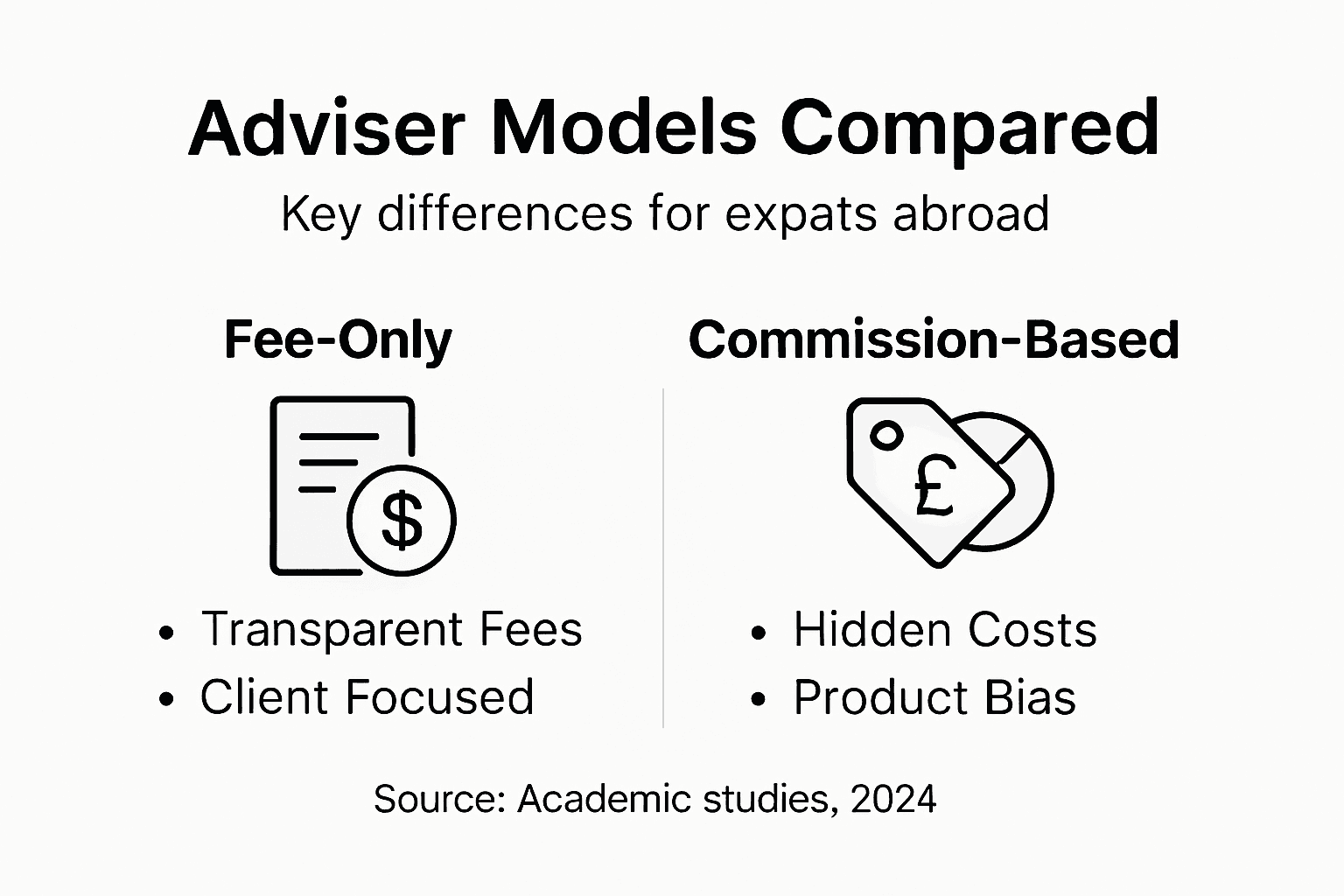

Advantages of Fee-Only Advisers | Fee-only financial advisers offer transparent, unbiased advice by eliminating incentives tied to product sales, ensuring alignment with client interests. |

Commission-Based Advice Explained Clearly

Commission-based financial advice operates on a compensation model that fundamentally challenges consumer interests. Under this arrangement, financial advisers earn money by selling specific financial products, creating an inherent conflict of interest that can significantly impact the quality of guidance provided to expatriates and international investors.

The core mechanism of commission-based advice involves advisers receiving payments directly from product providers based on the volume or type of financial products they sell. Financial incentives can distort advisor recommendations in ways that might not align with a client’s best financial outcomes. This means an adviser could potentially recommend a high-commission investment product that generates substantial personal income but provides suboptimal returns for the client.

Key characteristics of commission-based financial advice include:

Compensation tied directly to product sales

Potential bias towards higher-commission financial instruments

Limited transparency about underlying motivations

Reduced fiduciary responsibility to the client

Higher likelihood of recommending complex or unnecessary products

Research from academic studies reveals significant problems with commission structures that incentivise advisers to prioritise their financial gains over client welfare. These structures can lead to recommendations that generate maximum commissions rather than optimal financial strategies for international investors.

Pro tip: Always request a complete breakdown of an adviser’s compensation structure and potential conflicts of interest before engaging their services.

Types of Adviser Fee Structures Compared

Financial advisers employ several distinct fee structures that dramatically impact the quality and objectivity of financial guidance. Understanding these structures is crucial for expatriates seeking transparent, client-focused financial advice across international markets.

The most prevalent advisory fee models include various compensation approaches that fundamentally differ in their alignment with client interests. These range from asset-based fees and hourly charges to flat rates, retainer models, and commission-based compensation.

Key fee structures for international financial advisers include:

Asset Under Management (AUM) Fees

Percentage-based charge (typically 0.5-1.5%)

Compensation directly tied to portfolio size

Incentivises portfolio growth

Hourly Consultation Fees

Fixed rate per hour of professional time

Transparent billing

Best for specific, targeted financial planning

Flat Fee Structures

Predetermined fixed cost for services

Predictable expenses

Less dependent on portfolio complexity

Performance-Based Fees

Compensation linked to investment returns

Potentially higher risk/reward scenario

Less common in regulated markets

Commission-Based Compensation

Payment from product sales

Highest potential conflict of interest

Least transparent approach

Pro tip: Request a comprehensive fee breakdown and conflict of interest disclosure before engaging any financial adviser to ensure complete transparency.

Here’s a concise comparison of the main financial adviser fee models and who they suit best:

Fee Structure | Typical Client Scenario | Alignment with Client Interest | Cost Predictability |

Asset Under Management | Ongoing portfolio management | Generally high | Moderate, varies with assets |

Hourly Consultation | One-off financial questions | High | High, pay-as-you-go |

Flat Fee | Comprehensive financial planning | High | Very high, fixed charge |

Performance-Based | Aggressive investment strategies | Mixed, may encourage risk | Variable, based on returns |

Commission-Based | Product-focused sales | Low, prone to conflicts | Low upfront, costly in long run |

How Commissions Create Conflicts of Interest

Commission-based financial advice introduces a fundamental structural problem that can seriously compromise the quality of financial guidance provided to international investors. The inherent design of commission compensation creates powerful incentives that may not align with a client’s best financial interests.

Conflicts of interest emerge when advisers receive financial incentives that prioritise product sales over client outcomes. These incentive structures fundamentally distort the advisory relationship, pushing advisers towards recommending financial products that generate the highest commissions rather than those most suitable for the client’s specific financial situation.

The key mechanisms through which commissions create conflicts include:

Product Bias

Prioritising high-commission financial products

Steering clients towards unnecessary or complex investments

Recommending proprietary products over more suitable alternatives

Quantity Over Quality

Incentivising frequent trading

Encouraging unnecessary portfolio restructuring

Generating revenue through transaction volumes

Disclosure Limitations

Minimal transparency about compensation structures

Incomplete information about product risks

Potential concealment of alternative investment options

Suitability vs Fiduciary Standards

Meeting only basic ‘suitability’ requirements

Lower legal obligation to act in client’s best interests

Reduced accountability for suboptimal recommendations

Commission structures fundamentally compromise the adviser’s ability to provide truly independent financial guidance.

Some European regulators have already taken decisive action. Regulatory bans on commissions have demonstrated significant improvements in financial advice quality, promoting more transparent and client-focused advisory practices.

Pro tip: Always request a comprehensive breakdown of an adviser’s compensation structure and potential conflicts of interest before engaging their services.

Hidden Costs and Long-Term Financial Impact

Commission-based financial advice carries profound hidden costs that can silently erode investment returns and compromise long-term financial strategies. International investors particularly face significant risks when engaging advisers compensated through product sales rather than transparent fee structures.

Financial adviser remuneration through commissions consistently biases product recommendations towards higher-fee investments that generate maximum compensation. This systematic bias can substantially reduce portfolio performance and diminish wealth accumulation over decades of investment.

The multilayered financial consequences of commission-based advice include:

Reduced Investment Returns

Higher embedded product fees

Unnecessary portfolio complexity

Suboptimal asset allocation

Compounding Cost Implications

Incremental fees accumulate exponentially

Significant long-term wealth erosion

Reduced retirement fund potential

Strategic Recommendation Distortions

Prioritising commission-generating products

Overlooking more cost-effective alternatives

Potential misalignment with investor goals

Psychological Investment Barriers

Reduced trust in financial advice

Increased investor scepticism

Potential disengagement from professional guidance

Commission structures can silently drain up to 30% of potential investment growth over typical investment lifecycles.

Transparent, fee-only advisory models represent a critical evolution in protecting investor interests, ensuring recommendations are driven by client needs rather than sales incentives. By eliminating hidden commissions, investors gain clearer, more objective financial guidance.

Pro tip: Request a detailed breakdown of all potential investment fees and compare total cost structures across multiple advisers before making a commitment.

Cross-Border Risks for American Expats

American expatriates navigating international financial landscapes face a complex array of unique challenges that can dramatically impact their long-term financial security. The intersection of multiple regulatory environments, tax systems, and investment frameworks creates potential pitfalls that require sophisticated, specialised guidance.

Cross-border financial planning demands comprehensive understanding of intricate international regulations that differ significantly from domestic investment strategies. Expatriates must carefully negotiate nuanced legal and financial requirements that can vary dramatically between the United States and their new country of residence.

Key cross-border risks for American expats include:

Taxation Complexity

Dual reporting requirements

Potential double taxation scenarios

Intricate foreign income reporting obligations

Investment Restrictions

Limitations on US-based investment products

Potential tax inefficiencies in foreign markets

Restricted access to certain financial instruments

Retirement Account Challenges

Complications with 401(k) and IRA management

Potential tax penalties for international transfers

Complex rules surrounding pension contributions

Regulatory Compliance Risks

Differing financial reporting standards

Potential legal and financial penalties

Complex documentation requirements

International financial strategies require more than standard domestic financial planning.

Understanding these risks requires a nuanced approach that combines deep knowledge of both American and international financial systems. Professional guidance becomes crucial in navigating these complex regulatory landscapes.

Pro tip: Consult a specialised cross-border financial adviser with proven expertise in US expatriate financial planning before making any significant international financial decisions.

Benefits of Choosing Fee-Only Financial Advisers

Fee-only financial advisers represent a transformative approach to financial planning that prioritises client interests over sales commissions. By eliminating product-based incentives, these professionals provide a transparent, unbiased pathway to achieving complex financial objectives for international investors.

Fee-only advisers operate under strict fiduciary standards that legally mandate acting in their clients’ best interests. This fundamental difference distinguishes them from commission-based advisers who may be motivated by product sales rather than holistic financial strategies.

Key advantages of fee-only financial advisers include:

Transparency

Clear, upfront fee structures

No hidden sales commissions

Predictable pricing models

Unbiased Recommendations

Advice based on client needs

Comprehensive investment analysis

No product sales incentives

Comprehensive Financial Planning

Holistic approach to wealth management

Strategic long-term financial guidance

Personalised investment strategies

Fiduciary Commitment

Legal obligation to prioritise client interests

Highest standard of professional ethics

Comprehensive financial risk management

Fee-only advisers align their success directly with their clients’ financial growth.

These professionals provide a sophisticated alternative to traditional commission-based models, offering nuanced, client-focused financial guidance that transcends simple product recommendations.

The following table highlights how fee-only and commission-based advisers differ across critical factors for international investors:

Feature | Fee-Only Adviser | Commission-Based Adviser |

Payment Source | Direct client payment | Product provider commissions |

Advice Objectivity | Unbiased, client-focused | Prone to product sales bias |

Transparency | Full disclosure of costs | Limited fee visibility |

Regulatory Standard | Fiduciary duty | Often suitability only |

Pro tip: Always verify an adviser’s fee structure and fiduciary status before engaging their services to ensure complete transparency and alignment of interests.

Secure Transparent Cross-Border Financial Advice Without Hidden Commissions

Navigating international finances as an American expatriate can feel overwhelming, especially when facing commission-based advice that conflicts with your best interests. This article clearly highlights how commissions create biases and hidden costs that silently erode your investment growth. If you demand unbiased, fee-only guidance tailored to your unique cross-border needs, it is crucial to connect with advisers you can trust.

At Linkindependent.com, we simplify your search for verified, regulated financial professionals committed to transparency and fiduciary responsibility. Whether you need expert help managing 401ks, pensions, tax planning, or wealth strategies in Europe or beyond, our personalised matching ensures you find advisers who prioritise your financial wellbeing over product commission. Act now to avoid costly conflicts of interest and secure a clear, objective path to international wealth management. Discover trusted experts and book your free consultation today at Linkindependent.com.

Frequently Asked Questions

What is commission-based financial advice?

Commission-based financial advice is a compensation model where advisers earn fees by selling specific financial products, which may create conflicts of interest and lead to biased recommendations that don’t necessarily prioritise the client’s best financial outcomes.

How do commission structures affect the objectivity of financial advice?

Commission structures can distort the advisory relationship by incentivising advisers to recommend higher-commission products rather than the most suitable options for the client, potentially leading to suboptimal financial strategies.

What are the risks of engaging a commission-based adviser?

Engaging a commission-based adviser can result in reduced investment returns, hidden costs that can erode wealth over time, and recommendations that may not align with your financial goals due to the adviser’s financial incentives.

Why should I choose a fee-only financial adviser instead?

Fee-only financial advisers operate under a fiduciary duty, providing unbiased advice based solely on client needs. This approach ensures transparency, as clients are informed about all fees upfront, and reduces the risk of conflicts of interest associated with commission-based structures.

Recommended

Comments