Why Choose Regulated Financial Advisers: Global Impact

- Dec 18, 2025

- 7 min read

Over 80 percent of British adults have sought financial guidance, yet many are unaware of the substantial difference between regulated and unregulated advisers. When it comes to making choices about your hard-earned money, knowing who is truly qualified can save you from costly mistakes. Understanding what sets regulated financial advisers apart empowers you to demand higher standards, protect your finances, and secure support backed by the rigorous frameworks that British regulations provide.

Table of Contents

Key Takeaways

Point | Details |

Regulated Advisers Prioritise Client Interests | Regulated financial advisers must adhere to strict ethical guidelines and legal standards, ensuring they provide personalised recommendations that align with their clients’ best interests. |

Professional Accreditation Ensures Quality | Only authorised advisers with specific qualifications can operate, ensuring clients receive expert advice backed by ongoing professional development and compliance checks. |

Legal Protections Against Misconduct | Clients are financially protected by mandatory professional indemnity insurance, allowing them recourse in cases of inappropriate or negligent advice. |

Understanding Adviser Types is Crucial | Clients should distinguish between independent and restricted advisers to ensure they receive impartial advice tailored to their unique financial situations. |

Regulated financial advisers explained clearly

Financial regulation represents a critical safeguard protecting consumers from potential professional misconduct. Regulated financial advice involves personalized recommendations provided by authorized professionals who must adhere to stringent legal standards and ethical guidelines. These professionals are not simply salespeople, but highly trained experts obligated to prioritise their clients’ best financial interests.

Key characteristics distinguish regulated financial advisers from unregulated practitioners. Authorized professionals must maintain specific qualifications, undergo regular compliance checks, and demonstrate comprehensive knowledge across complex financial domains. They are legally required to provide transparent advice, disclose potential conflicts of interest, and maintain professional indemnity insurance. This means if an adviser provides inappropriate guidance, clients have legal recourse and financial protection.

The regulatory framework ensures advisers follow strict protocols designed to protect consumers. Financial adviser regulations mandate comprehensive documentation, detailed risk assessments, and ongoing professional development. Advisers must continuously update their knowledge, track market changes, and adapt their strategies to evolving financial landscapes. This commitment to professional standards guarantees clients receive sophisticated, current, and responsible financial guidance.

Pro Tip: Always verify an adviser’s regulatory status by requesting their official registration number and cross-checking with national financial regulatory bodies before committing to any financial recommendations.

Types of regulated advisers and specialisms

Independent financial advisers (IFAs) represent a crucial category of financial professionals offering comprehensive, unbiased advice across multiple financial products and investment strategies. These advisers operate with a holistic approach, examining clients’ entire financial landscape rather than pushing specific products or narrow investment recommendations.

Specialised financial adviser categories include wealth management experts, retirement planning specialists, and international investment consultants. Commodity Trading Advisors (CTAs) provide niche expertise in futures contracts and commodity options, operating under stringent regulatory frameworks. Other specialist advisers focus on specific domains such as pension transfers, inheritance tax planning, investment portfolio management, and cross-border financial strategy.

The regulatory landscape distinguishes between two primary adviser types: independent and restricted practitioners. Independent financial advisers can recommend products from across the entire market, ensuring clients receive truly impartial guidance. Restricted advisers, by contrast, offer recommendations limited to specific providers or product ranges. This distinction is critical for clients seeking transparent, comprehensive financial planning that aligns precisely with their unique economic circumstances and long-term objectives.

This table summarises key specialisms and their typical focus areas:

Adviser Specialism | Main Areas of Expertise | Typical Client Benefit |

Independent Financial Advisers | Full-market analysis, investment suites | Impartial, broad-based solutions |

Wealth Management Experts | Asset growth, portfolio strategy | Tailored wealth optimisation |

Retirement Planning Specialists | Pension schemes, income strategies | Secure retirement income planning |

Commodity Trading Advisors | Futures, commodity options | Specialist market participation |

Pro Tip: Research an adviser’s specific regulatory permissions and specialisms before engaging their services, ensuring their expertise matches your precise financial requirements and investment goals.

Core safeguards: compliance and accountability

Regulatory frameworks play a critical role in defining financial advice standards, ensuring firms provide transparent, accountable services that protect consumers from potentially misleading information. These comprehensive guidelines establish minimum professional requirements, mandating that financial advisers maintain the highest levels of ethical conduct and technical competence.

The accountability mechanisms extend far beyond simple documentation. Professional regulatory bodies impose strict compliance protocols that require advisers to demonstrate ongoing professional development, maintain comprehensive client records, and submit to regular independent audits. Financial Advisory and Intermediary Services regulations mandate detailed reporting processes, ensuring advisers cannot operate without continuous professional scrutiny and demonstrable competence in their respective financial domains.

Key safeguards include mandatory professional indemnity insurance, which protects clients from potential financial losses resulting from inappropriate advice, and rigorous qualification standards that demand continuous education and skill verification. Advisers must regularly update their knowledge, pass professional examinations, and maintain transparent communication channels with both regulatory authorities and their clients. These multilayered accountability mechanisms create a robust ecosystem of trust, competence, and consumer protection.

Pro Tip: Always request and independently verify an adviser’s current regulatory credentials, including their professional registration number and most recent compliance audit documentation, before entering into any financial engagement.

Risk protection and legal responsibilities

Legal obligations for financial advisers represent a comprehensive framework designed to protect clients from potential financial risks and professional misconduct. These statutory requirements mandate that regulated advisers must provide accurate, transparent, and personalised recommendations that demonstrably serve their clients’ best financial interests, with significant legal consequences for failing to meet these standards.

The legal accountability mechanisms extend across multiple dimensions of financial advisory practice. Advisers are required to maintain professional indemnity insurance, which provides financial protection for clients in scenarios where inappropriate or negligent advice leads to monetary losses. This insurance acts as a critical safeguard, ensuring clients have recourse and potential compensation if an adviser’s recommendations result in demonstrable financial damage.

Regulatory frameworks impose stringent documentation and disclosure requirements, compelling advisers to maintain comprehensive records of all client interactions, recommendations, and the rationale behind specific financial strategies. These detailed documentation protocols create an audit trail that protects both the client and the adviser, enabling precise reconstruction of advisory processes and ensuring transparent decision-making. The legal responsibilities encompass ongoing duty of care, requiring continuous monitoring and potential adjustment of financial recommendations as clients’ circumstances and market conditions evolve.

Pro Tip: Request a detailed written statement explaining an adviser’s specific legal responsibilities, professional indemnity coverage, and complaint resolution processes before finalising any financial engagement.

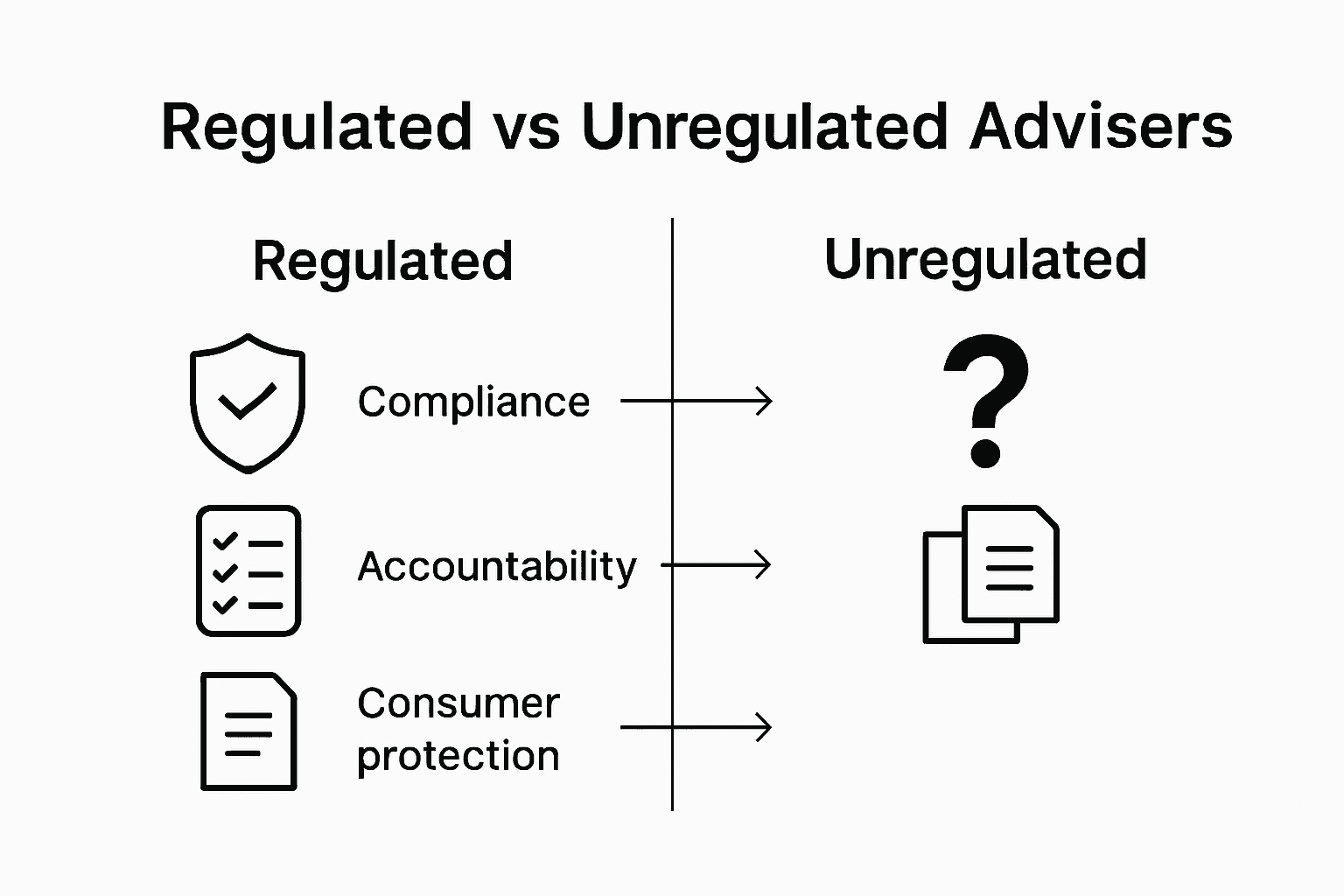

Comparing regulated and unregulated advisers

Financial advice regulations create a fundamental distinction between regulated and unregulated financial advisers, establishing critical protections for consumers navigating complex financial landscapes. Regulated advisers operate within strict legal frameworks that mandate personalised, accountable recommendations, whereas unregulated practitioners can offer generic guidance without comparable professional obligations.

The key differentiators between these advisory categories are profound and multifaceted. Regulated advisers must maintain comprehensive professional credentials, undergo continuous training, carry professional indemnity insurance, and adhere to stringent ethical standards. Unregulated advisers face no such requirements, which means clients engaging with them assume significantly greater personal risk. The absence of mandatory qualifications, ongoing professional development, and legal accountability creates potential vulnerabilities for unsuspecting investors.

Practical implications of this regulatory divide extend beyond mere paperwork. Regulated advisers are legally compelled to prioritise clients’ financial interests, provide transparent documentation, and offer clear recourse mechanisms if recommendations prove inappropriate. Unregulated advisers operate with minimal oversight, potentially dispensing advice based on personal interests or limited understanding. This fundamental difference means regulated professionals must maintain detailed records, justify their recommendations, and face professional consequences for misconduct, whereas unregulated advisers can potentially provide advice without substantive consequence.

Here is a concise comparison of regulated versus unregulated financial advisers:

Criteria | Regulated Advisers | Unregulated Advisers |

Professional Qualifications | Must hold certified credentials | No mandatory qualifications |

Legal Accountability | Legally bound, face sanctions for misconduct | No enforceable legal accountability |

Client Protection | Offer financial recourse and insurance cover | No guaranteed financial safeguards |

Advice Approach | Personalised, needs-based recommendations | General, often unverified suggestions |

Pro Tip: Always verify an adviser’s regulatory status by requesting their official registration number and cross-referencing it with the relevant national financial regulatory authority before engaging their services.

Connect with Verified Regulated Financial Advisers for Your Global Needs

Choosing regulated financial advisers is essential when handling complex international finances and seeking trustworthy guidance that puts your best interests first. This article highlights key challenges such as verifying adviser credentials, understanding legal protections, and navigating cross-border financial regulations. At Linkindependent.com we simplify these concerns by connecting you with fully compliant, credentialed professionals across wealth planning, international mortgages, and tax strategies. Our platform ensures transparency and independence so you can feel confident your financial future is in expert hands.

Take control of your international financial decisions today by accessing our network of trusted advisers. Define your needs, receive personalised matches, and schedule free consultations with advisers verified for their regulatory status and specialised expertise. Don’t risk costly mistakes with unregulated guidance. Visit Linkindependent.com now to find your ideal financial partner and secure peace of mind in managing your global wealth. Your long-term success starts with informed, regulated advice.

Frequently Asked Questions

What is a regulated financial adviser?

A regulated financial adviser is a professional who provides personalized financial advice while adhering to strict legal standards and ethical guidelines, ensuring that clients’ best financial interests are prioritised.

What are the benefits of choosing a regulated financial adviser?

Choosing a regulated financial adviser ensures comprehensive consumer protection, including legal recourse and professional indemnity insurance, which safeguards clients against potential losses from inappropriate financial advice.

How do regulated financial advisers differ from unregulated advisers?

Regulated financial advisers must hold specific qualifications and maintain ongoing compliance with legal frameworks, while unregulated advisers have no formal requirements or accountability, making clients more vulnerable to poor advice.

What types of services do regulated financial advisers offer?

Regulated financial advisers offer a wide range of services, including investment planning, wealth management, retirement planning, and specialised support in areas like inheritance tax and pension transfers.

Recommended

Comments