Why personalised advice is essential for US expats in Europe

- 2 days ago

- 8 min read

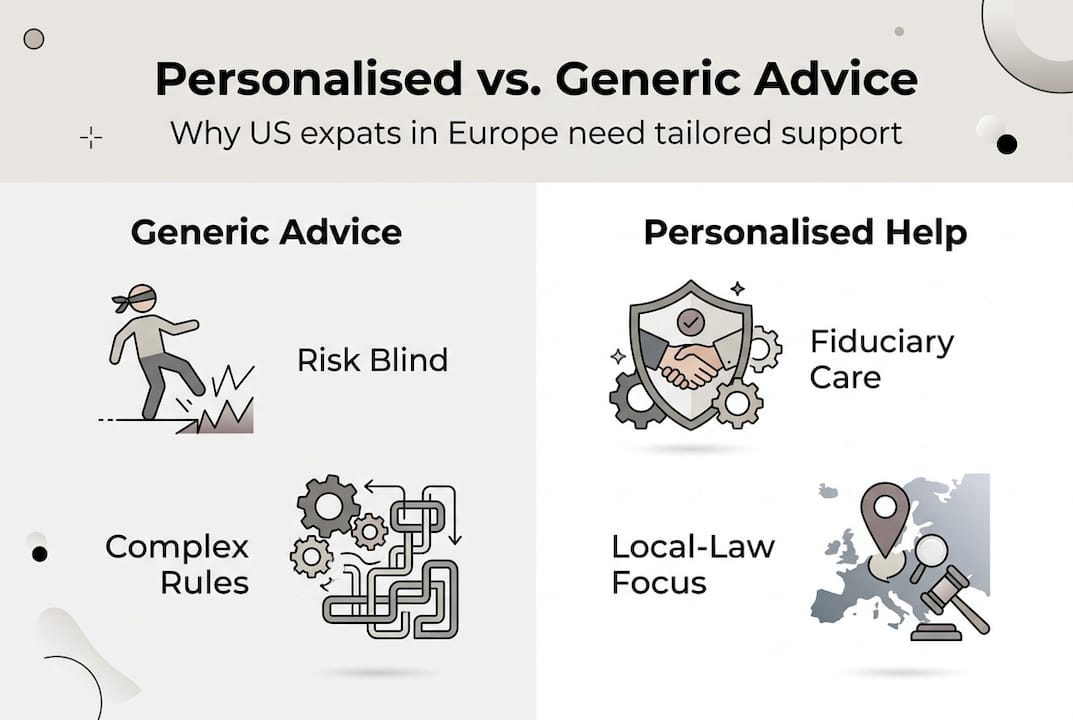

Moving to Europe as a US citizen is exciting. But the financial complexity that comes with it is genuinely serious. Many Americans assume that a quick search online or a chat with their existing US adviser is enough to prepare them. It rarely is. Estate planning alone varies so dramatically across EU countries that a will valid in the US may be entirely unenforceable in France or Spain. Cross-border rules touch everything from how your investments are taxed to who legally inherits your assets. Generic advice, however well-intentioned, simply cannot account for that level of complexity. Personalised guidance from verified, cross-border specialists is not a luxury. It is a necessity.

Table of Contents

Key Takeaways

Point | Details |

Generic advice is risky | Relying on non-specialist financial advice can result in costly mistakes for US expats in Europe. |

Personalised guidance prevents errors | Expert advice tailored to your unique situation addresses complex cross-border tax and estate issues. |

Early planning is vital | Strategic, early planning secures the best outcomes and avoids irreversible mistakes before and after relocating. |

Fiduciary specialists add value | Qualified, conflict-free experts ensure full compliance and alignment with both US and EU laws. |

Action means security | Taking practical steps now delivers future financial security and peace of mind as you move abroad. |

Why generic advice falls short for US expats

The European Union is not a single financial jurisdiction. Each member state has its own tax laws, residency rules, reporting obligations, and investment restrictions. What works in Germany may be entirely wrong for Portugal. This is why personalised expat advice is so critical. A one-size-fits-all approach simply cannot account for the legal and regulatory diversity you will encounter.

Take Spain as a clear example. Spain requires foreign residents to file the Modelo 720, a declaration of overseas assets exceeding €50,000. Missing this filing can result in severe penalties. Generic advice ignores country-specific obligations like this entirely, leaving you exposed to fines you never saw coming.

Beyond reporting, generic guidance also misses investment restrictions. Many US-domiciled funds are classified as Passive Foreign Investment Companies (PFICs) under EU rules, making them highly tax-inefficient for European residents. A standard US broker will rarely flag this.

As one cross-border specialist put it:

“Rigid financial plans built without local knowledge are not just unhelpful. They are actively dangerous for US citizens relocating abroad. Your plan must evolve as your life and your legal environment change.”

Personal and family circumstances add another layer. Whether you are married to a European national, have children from a previous relationship, or own property in multiple countries, your situation demands a flexible plan. International estate planning must be built around your specific life, not a template.

Key reasons generic advice fails US expats:

It ignores country-specific reporting requirements such as Spain’s Modelo 720

It overlooks PFIC rules that make US funds tax-inefficient in Europe

It fails to account for residency-based tax triggers in your destination country

It cannot adapt to your personal family structure or asset profile

It treats the EU as a single market when it is legally 27 separate ones

The risks of cross-border financial mistakes

Understanding why generic advice falls short is one thing. Seeing the real-world consequences of acting on it is another. The financial and legal risks for US expats who do not plan carefully are significant and, in some cases, irreversible.

Here are five of the most common and costly mistakes:

Failing to declare overseas assets. Missing filings like the Modelo 720 or FBAR (Foreign Bank Account Report) can trigger penalties of tens of thousands of dollars.

Mishandling US trusts in Europe. Many EU countries do not recognise US trusts, meaning your carefully structured estate plan may be legally void the moment you establish residency abroad.

Ignoring forced heirship laws. Several EU countries legally require a portion of your estate to pass to specific relatives, regardless of what your will says.

Holding US-domiciled investments. Keeping funds in US-based accounts after relocating can trigger punishing tax treatment under both US and European rules simultaneously.

Delaying tax election decisions. Choosing between the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit (FTC) has long-term consequences. Getting it wrong early locks you into a costly position.

The financial stakes are real. In some EU jurisdictions, inheritance tax thresholds are far lower than in the US, and combined tax rates on estates can exceed 50% without proper structuring. Proactive estate planning guidance and early engagement with multi-jurisdictional wealth planning specialists can prevent these outcomes entirely.

Pro Tip: Engage both a US-qualified tax adviser and a local European specialist at least 12 months before your move. Do not wait until you have already relocated to start mapping out your legal obligations. By then, some decisions will already be locked in.

Solid international tax planning is not about avoiding tax. It is about structuring your affairs correctly so you pay what you owe in the right jurisdiction, at the right time, without duplication or penalty.

How personalised financial advice resolves these challenges

Now that the risks are clear, the solution becomes straightforward. Personalised advice from a fiduciary Registered Investment Adviser (RIA) with genuine cross-border experience is the most reliable way to protect your financial future as a US expat in Europe.

The difference between a generic broker and a fiduciary adviser for expats is not subtle. It is fundamental.

Feature | Generic broker | Fiduciary RIA with expat experience |

Legal obligation to client | None (suitability standard only) | Full fiduciary duty |

Cross-border specialism | Rarely available | Core competency |

Conflict of interest | Common (commission-based) | Minimal (fee-only structure) |

Outcome alignment | Product-driven | Client-goal-driven |

Regulatory compliance across borders | Limited | Actively managed |

Research confirms that cross-border planning needs fiduciary RIAs with genuine expat experience, not generic brokers whose incentives may not align with yours. This is not a minor distinction when your retirement savings, property, and inheritance are all at stake.

The benefits of truly personalised advice include:

Compliance assurance across both US and European tax systems

Flexible planning that adapts as your residency status or family situation changes

Local adaptation to the specific rules of your destination country

Coordinated strategy across tax, estate, and investment planning

Proactive risk management before problems arise, not after

The most effective approach involves a multi-disciplined team. Tax specialists, estate lawyers, and investment planners working together produce far better outcomes than any single adviser working in isolation. When choosing financial advisers abroad, always ask whether they can coordinate with other specialists across jurisdictions. If they cannot, keep looking. An international law firm with cross-border expertise is often a valuable part of that team.

The critical timing for expat financial planning

Knowing what to do is only half the equation. Knowing when to act is equally important. The window for optimal financial planning opens 12 to 24 months before your move. Miss it, and some of your most important decisions become far more expensive to reverse.

Stage | Timeline | Key actions | Risk if delayed |

Pre-move planning | 12 to 24 months before | Tax election review, estate restructuring, investment audit | Locked into costly US tax positions |

Transition period | 3 to 6 months before | Open European accounts, transfer assets, update wills | Compliance gaps at point of residency |

Post-move stabilisation | First 12 months abroad | File dual returns, confirm residency status, review pension | Penalties for missed filings |

Early planning of 12 to 24 months before your move allows you to make strategic elections between the FEIE and FTC, avoiding the locked five-year commitments that catch many expats off guard. Post-move, many US brokerage accounts impose restrictions on non-US residents, making proactive transitions essential.

Here are four steps to take as soon as possible:

Audit your current financial position. List all assets, accounts, pensions, and investments. Know what you hold and where before any adviser can help you effectively.

Identify your destination country’s rules. Each EU country has different residency triggers, tax treaties, and estate laws. Research yours specifically.

Engage a cross-border specialist team. Find advisers qualified in both US and European financial law. Do not rely on a single-country expert.

Review and update all estate documents. Wills, trusts, and beneficiary designations may need to be restructured entirely for your new country of residence.

Pro Tip: Start co-ordinating with both your US and European specialists simultaneously, not sequentially. Waiting for one to finish before engaging the other wastes months you cannot afford to lose.

The essential financial planning steps you take now will determine how smoothly your transition goes. Failing to act early does not just delay your planning. It locks in commitments and costs that could have been avoided entirely. Explore the wealth planning benefits available to US expats who plan ahead, and review essential advice for expats to understand what a well-structured plan actually looks like in practice.

Expert help for your relocation: why choose us

Everything covered in this article points to one clear conclusion. You need verified, experienced, cross-border specialists in your corner before you move. At Linkindependent.com, we connect US citizens relocating to Europe with a trusted network of regulated financial advisers, tax professionals, and estate planning specialists who understand both sides of the Atlantic.

[

Our matching process is built around your specific situation, not a generic list. Every adviser in our network is verified, regulated, and experienced in cross-border financial planning for US expats. We prioritise fiduciary-first advice with transparent fee structures, so you always know exactly who you are working with and why. Whether you need help with tax elections, pension transfers, estate restructuring, or investment compliance, we can connect you with the right expert. Book a free consultation today and take the first step towards a financially secure life in Europe.

Frequently asked questions

What makes financial advice truly personalised for US expats?

True personalisation means advice built around your life stage, financial profile, and the legal specifics of both your US status and your European destination country. Generic advice ignores individual circumstances and country-specific laws entirely, which is where costly mistakes begin.

Why is timing so important for financial planning before expatriation?

Acting early allows you to make strategic US tax elections and restructure assets before residency triggers lock you into less favourable positions. Early planning of 12 to 24 months before your move is the recognised benchmark for avoiding costly, locked-in commitments.

How do EU estate laws affect Americans moving overseas?

EU estate rules frequently override US trusts and enforce forced heirship, meaning your existing will may not be legally valid in your new country of residence. Many EU countries reject US trusts outright, making dual-country legal co-ordination essential.

What is a fiduciary and why does it matter for US expats?

A fiduciary is legally obligated to act in your best interests at all times, unlike a standard broker who only needs to recommend suitable products. For US expats, cross-border planning demands fiduciary RIAs with genuine expat experience to avoid conflicts and ensure full compliance across jurisdictions.

Recommended

Comments