International business banking guide for US expats in Europe

- 2 days ago

- 8 min read

Running a business from Europe as a US citizen sounds exciting, and it genuinely is. But the financial complexity that comes with it catches many people off guard. Between FATCA reporting burdens, EU compliance rules, and the risk of choosing the wrong bank or investment structure, the stakes are high. Miss a filing deadline or open the wrong account, and you could face serious penalties or frozen funds. This guide walks you through the key steps: from gathering the right documents and choosing a compliant bank, to managing cross-border taxes, investments, and long-term wealth planning. Consider it your practical roadmap for getting it right from the start.

Table of Contents

Key Takeaways

Point | Details |

Prioritise expat-friendly banks | Choose banks that support US expats and comply with FATCA, like Wise and HSBC Expat. |

Understand your reporting duties | Stay compliant by filing FBAR, FATCA, and using FEIE or FTC for optimal tax results. |

Investments require US focus | Avoid EU-domiciled funds due to punitive taxes; prefer US-domiciled options and seek specialist advice. |

Layer your liquidity | Keep both EUR and USD accounts open for flexibility and estate planning advantages. |

Key prerequisites: what you need to know before opening an account

Before you approach any bank, preparation is everything. European banks have become increasingly cautious about US clients, and for good reason. The Foreign Account Tax Compliance Act (FATCA) places significant reporting obligations on non-US banks that hold accounts for American citizens. As a result, many EU banks reject or terminate US client accounts altogether. Viable options include HSBC Expat, Citibank IPB, and some digital EU business accounts that accept non-residents.

Knowing which documents to prepare in advance saves you weeks of back-and-forth. Most banks will require Know Your Customer (KYC) checks, which means proving your identity, address, and the legitimacy of your business.

Documents you will typically need:

Valid US passport and a secondary photo ID

Proof of European residency (rental contract, utility bill, or residence permit)

Business registration documents from your EU country of incorporation

US tax identification number (TIN) and recent IRS filings

FATCA self-certification form (W-9 or W-8BEN-E depending on entity type)

Proof of business activity (contracts, invoices, or a business plan)

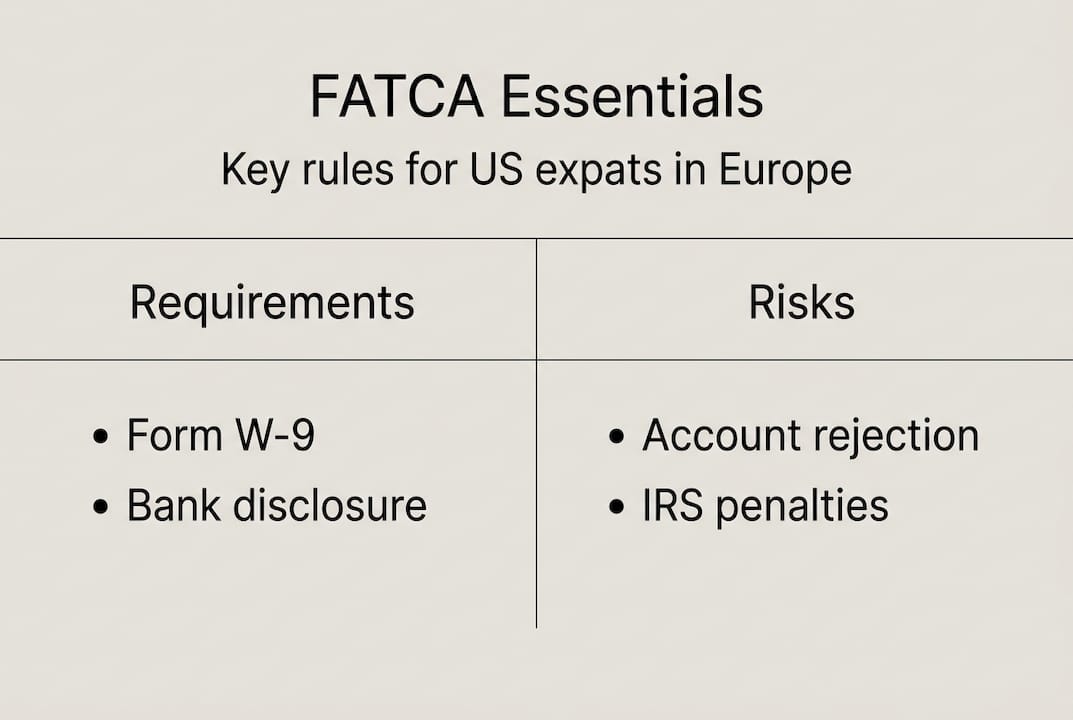

Understanding the FATCA requirements for US expats before you apply will help you anticipate questions and avoid rejections. The Common Reporting Standard (CRS) adds another layer, as EU banks also share account data with tax authorities across member states.

Bank type | FATCA acceptance | Setup speed | Best for |

HSBC Expat | Yes | Moderate | Established businesses |

Citibank IPB | Yes | Moderate | High-net-worth expats |

Revolut Business | Varies | Fast | Startups and SMEs |

Wise Business | Varies | Fast | Freelancers and SMEs |

Traditional EU bank | Often no | Slow | Local operations only |

For sound business wealth planning basics, getting your banking structure right at this stage is the foundation everything else is built upon.

Pro Tip: Digital-first banks are faster to set up, but always confirm their FATCA acceptance policy before applying. Some digital banks quietly restrict US-person accounts after onboarding, which creates real disruption.

Opening and managing international business banking accounts

Once your documents are in order, the process of opening an account becomes far more straightforward. The key is choosing a bank that genuinely supports cross-border operations, not just one that tolerates them.

Recommended banks for cross-border operations in Europe include Revolut Business, Wise Business, and Qonto. These platforms offer multi-currency accounts, low foreign exchange fees, and local IBANs, making them well suited to small and medium-sized enterprises (SMEs) and expat-owned businesses.

Steps to open and manage your business account:

Choose a bank that explicitly accepts US-person business accounts and supports FATCA compliance.

Gather all required KYC and business documents before starting your application.

Apply online or in branch, completing all FATCA self-certification forms accurately.

Activate your account and set up multi-currency wallets for EUR, USD, and any other currencies you trade in.

Segregate business and personal funds immediately. Never mix the two.

Set up automated reconciliation and accounting integrations where possible.

Review your account terms annually, as FATCA policies at digital banks can change.

Feature | Digital banks | Traditional banks |

Multi-currency accounts | Yes | Limited |

Local IBANs | Yes | Yes |

FX fees | Low (0.5% or less) | Higher (1.5%+) |

FATCA acceptance | Variable | More consistent |

Setup time | 1 to 3 days | 2 to 6 weeks |

Business credit options | Limited | Broader |

For more practical cross-border business account tips, consider how your banking structure will interact with your VAT obligations and payroll requirements. Some countries require a local IBAN for VAT direct debits, which makes multi-IBAN accounts particularly valuable.

You can also explore global bank recommendations to compare options across jurisdictions before committing.

Pro Tip: Prioritise banks that allow multiple IBANs within one account. This lets you ring-fence VAT collections, payroll, and operating funds cleanly, which simplifies your tax reporting considerably.

Navigating cross-border tax requirements and reporting

With your banking in place, tax compliance becomes your most pressing ongoing responsibility. As a US citizen, you are taxed on your worldwide income regardless of where you live. That means you must file both US and EU tax returns every year, and the two systems do not always align neatly.

The two main tools for reducing double taxation are the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit (FTC). FEIE excludes up to $130,000 in foreign earned income for 2025 (filed in 2026) if you qualify via the physical presence test (330 days abroad) or bona fide residence. FTC credits foreign taxes paid, dollar for dollar, against your US liability. You can learn more about how to use FEIE and FTC to decide which approach suits your situation.

Cross-border tax tasks in sequence:

Determine your tax residency status in your EU country of residence.

Register your business with the local tax authority and obtain a VAT number if required.

File your EU income tax return according to local deadlines (typically April to June).

File your US federal return by 15 April, or use the automatic 15 June expat extension.

File FinCEN 114 (FBAR) by 15 April, with an automatic extension to 15 October.

File IRS Form 8938 (FATCA) if your foreign assets exceed the relevant threshold.

Apply FEIE or FTC to reduce your US tax liability on foreign income.

Common tax mistakes to avoid:

Failing to file FBAR when aggregate foreign accounts exceed $10,000 at any point in the year

Applying FEIE and FTC to the same income, which is not permitted

Missing the FATCA Form 8938 threshold: foreign assets over $200,000 at year-end (or $300,000 at peak) trigger filing requirements for expats abroad

Investing in EU-domiciled funds without understanding Passive Foreign Investment Company (PFIC) rules

Ignoring state tax obligations if your home state still considers you a resident

Non-willful FBAR penalties start at $10,000 per year per account. Willful violations can reach the greater of $100,000 or 50% of the account balance. These are not theoretical risks. The IRS actively pursues non-compliant expats.

For effective cross-border tax planning, working with a specialist who understands both US and EU tax law is not optional. It is essential.

Investment, liquidity management, and wealth planning for expat businesses

Once your tax obligations are under control, building a sound investment and liquidity strategy protects your business and your personal wealth over the long term.

The single biggest investment trap for US expats in Europe is buying EU-domiciled funds. EU-domiciled funds trigger PFIC rules under US tax law, requiring you to file IRS Form 8621 and face punitive tax treatment on gains. EU PRIIPs (Packaged Retail and Insurance-based Investment Products) regulations also block US expats from purchasing many EU investment products, so the options are more limited than you might expect.

Preferred investment structures for US expats in Europe:

US-domiciled ETFs (exchange-traded funds) held through a US brokerage

Individual stocks on US exchanges

US-domiciled mutual funds

Multi-currency cash accounts for short-term liquidity

Real estate held in a tax-efficient structure

For compliant expat investment options, keeping your investment accounts with US-based brokers such as Schwab International or Interactive Brokers is generally the safest approach. Many US brokers still serve expats, and they understand the compliance landscape.

Liquidity management matters just as much as investment selection. Layered liquidity in EUR and USD, combined with maintaining open US accounts, gives you flexibility when currency markets shift or unexpected business costs arise. Europe is the largest source of foreign gross income for US expats, accounting for $87 billion or 23.9% of the total, which underlines just how significant the financial stakes are.

On the estate planning side, the US estate tax applies to worldwide assets. The exemption for 2025 sits at $13.61 million, but this is scheduled to reduce significantly after 2025 legislation expires. For cross-border wealth strategies, reviewing your estate structure with a qualified adviser now is far less costly than addressing it later.

Pro Tip: Use a cross-border financial adviser who holds licences in both the US and your EU country of residence. They can coordinate your banking, tax, and investment strategy as one integrated plan rather than three separate problems.

Why conventional expat banking advice falls short

Most articles about expat banking point you towards a digital bank, remind you to file your FBAR, and call it done. That advice is not wrong, but it is dangerously incomplete.

The reality is that digital banks are not a universal solution. Many quietly restrict or close US-person accounts when their compliance costs rise, leaving business owners scrambling mid-operation. FATCA risk is not a one-time hurdle at account opening. It is an ongoing relationship between your bank, the IRS, and your EU tax authority.

The most costly mistakes we see are not from people who ignored the rules entirely. They come from people who followed generic advice without understanding how banking, tax, and investment decisions interact. Choosing the wrong fund structure, for example, can create a PFIC problem that costs more to unwind than the original investment was worth.

Only a multi-jurisdictional advice specialist can see the full picture. They understand that your bank account choice affects your tax position, which affects your investment options, which affects your estate plan. Treating these as separate issues is where most expats go wrong.

Taking your next steps with expert guidance

Putting this knowledge into practice is where many expats stall. The rules are clear enough on paper, but applying them correctly to your specific business structure, country of residence, and personal financial goals requires specialist input.

[

At Linkindependent.com, we connect US expats in Europe with verified, regulated financial professionals who specialise in exactly this kind of cross-border complexity. Whether you need a licensed tax adviser, a cross-border wealth planner, or guidance on compliant banking structures, we match you with the right expert for your situation. Our process is simple: tell us what you need, we match you with a verified specialist, and you get a free initial consultation. Explore trusted financial advice tailored to your needs and take the guesswork out of managing your cross-border finances.

Frequently asked questions

Which European banks are expat-friendly for US-owned businesses?

Revolut Business, Wise Business, and Qonto are popular choices for their multi-currency features and SME focus, while HSBC Expat and Citibank IPB offer more consistent FATCA compliance for established businesses.

What are the biggest mistakes US expats make with business banking?

The most common errors include failing to file FBAR or FATCA forms on time, investing in EU-domiciled funds that trigger PFIC rules, and mixing personal and business funds in the same account.

How does FEIE differ from FTC for US expat business owners?

FEIE excludes up to $130,000 of foreign earned income from US tax, while FTC credits foreign taxes paid dollar for dollar. Use FEIE in lower-tax EU countries and FTC where local rates exceed US rates, but never apply both to the same income.

What are the penalties for missing FBAR or FATCA filings?

Non-willful FBAR penalties start at $10,000 per year, and willful violations can reach $100,000 or 50% of the account balance. FATCA non-compliance triggers additional IRS scrutiny and separate fines.

Recommended

Comments