Financial Adviser Regulatory Bodies Explained: Ensuring Global Trust

- Dec 8, 2025

- 6 min read

Regulatory bodies play a vital role in shaping how british financial advisers operate within a rapidly evolving global marketplace. With more than 60 countries relying on strict oversight, these institutions help protect investors and maintain public confidence in financial services worldwide. Understanding how key authorities, from the United Kingdom to Australia, enforce professional standards highlights why robust regulation matters for anyone seeking reliable financial advice today.

Table of Contents

Key Takeaways

Point | Details |

Importance of Regulatory Bodies | Financial adviser regulatory bodies are essential for establishing professional standards and protecting investors in global financial markets. |

Diverse International Frameworks | Regulatory approaches vary globally, reflecting different economic and legislative contexts, impacting how financial advisers operate. |

Client Protection Mechanisms | Comprehensive monitoring and risk management by regulatory bodies enhance investor protection and maintain professional conduct in the financial services industry. |

Risks of Unregulated Advice | Unregulated financial advice poses significant risks, including potential misconduct and exploitation of clients, necessitating robust oversight frameworks. |

Defining Financial Adviser Regulatory Bodies

Financial adviser regulatory bodies are critical institutions that establish and maintain professional standards within global financial services. These organisations play a pivotal role in protecting investors by ensuring financial advisers are professionally trained and regulated according to strict professional guidelines.

At the international level, regulatory frameworks are designed to create transparency and accountability. The International Organization of Securities Commissions (IOSCO) represents a prime example, working to develop comprehensive standards that enhance investor protection across global markets. Their mandate focuses on reducing systemic risk and promoting consistent professional practices among financial service professionals.

Key responsibilities of financial adviser regulatory bodies typically include:

Establishing minimum professional qualification requirements

Conducting background checks on financial professionals

Monitoring ongoing professional conduct and ethical standards

Investigating consumer complaints and potential misconduct

Maintaining public registers of licensed financial advisers

These organisations serve as crucial gatekeepers, creating structured pathways for professionals to demonstrate competence and maintain public trust. By implementing rigorous licensing processes and ongoing professional development requirements, they ensure that individuals managing complex financial portfolios meet highest industry standards. Investors can confidently seek guidance knowing these independent bodies provide robust oversight and protection in an increasingly sophisticated financial landscape.

Global Variations and Key Authorities

Regulatory approaches to financial adviser oversight demonstrate significant international diversity, reflecting unique economic landscapes and legislative frameworks. In France, for example, multiple regulatory bodies collaborate to ensure comprehensive financial service supervision, with the Prudential Supervisory and Resolution Authority (ACPR) overseeing banking and insurance sectors while the Financial Markets Authority (AMF) monitors investment services and market activities.

Across different regions, national regulatory frameworks exhibit distinctive characteristics. Some jurisdictions, like Mauritius, establish dedicated commissions to manage specific financial service domains. The Financial Services Commission (FSC) in Mauritius represents a targeted approach, concentrating on non-banking financial services including insurance, securities, private pensions, and global business sectors.

Key international regulatory authorities typically represent different models of financial oversight:

United Kingdom: Financial Conduct Authority (FCA)

United States: Securities and Exchange Commission (SEC)

European Union: European Securities and Markets Authority (ESMA)

Australia: Australian Securities and Investments Commission (ASIC)

Canada: Investment Industry Regulatory Organization of Canada (IIROC)

These organisations share fundamental objectives of investor protection, market stability, and professional standards enforcement. While methodologies vary, each regulatory body aims to create transparent, accountable financial ecosystems that balance innovation with robust consumer safeguards. Global financial advisers must navigate these complex, nuanced regulatory environments, demonstrating adaptability and comprehensive understanding of jurisdiction-specific requirements.

How Regulation Protects Clients Globally

Financial regulatory bodies play a critical role in protecting clients through comprehensive monitoring and proactive risk management strategies. The global financial protection framework extends far beyond simple oversight, creating robust mechanisms that safeguard investors’ interests across complex international financial landscapes.

At the international level, organisations like the Financial Stability Board (FSB) work tirelessly to develop comprehensive recommendations that enhance financial system stability and protect client interests. These institutions continuously assess potential risks, recommend policy improvements, and ensure that financial service providers maintain high standards of professional conduct.

Key client protection mechanisms include:

Mandatory professional qualifications and ongoing training requirements

Stringent background checks for financial professionals

Comprehensive complaint investigation procedures

Mandatory professional indemnity insurance

Regular financial audits and compliance checks

Transparency requirements for fee structures and potential conflicts of interest

These regulatory frameworks create multi-layered protection systems that address potential vulnerabilities before they impact individual investors. By establishing clear guidelines, enforcing professional standards, and maintaining active oversight, regulatory bodies significantly reduce the potential for financial misconduct. Clients can confidently engage financial advisers, knowing that sophisticated international mechanisms are continuously working to protect their financial interests and maintain the integrity of global financial services.

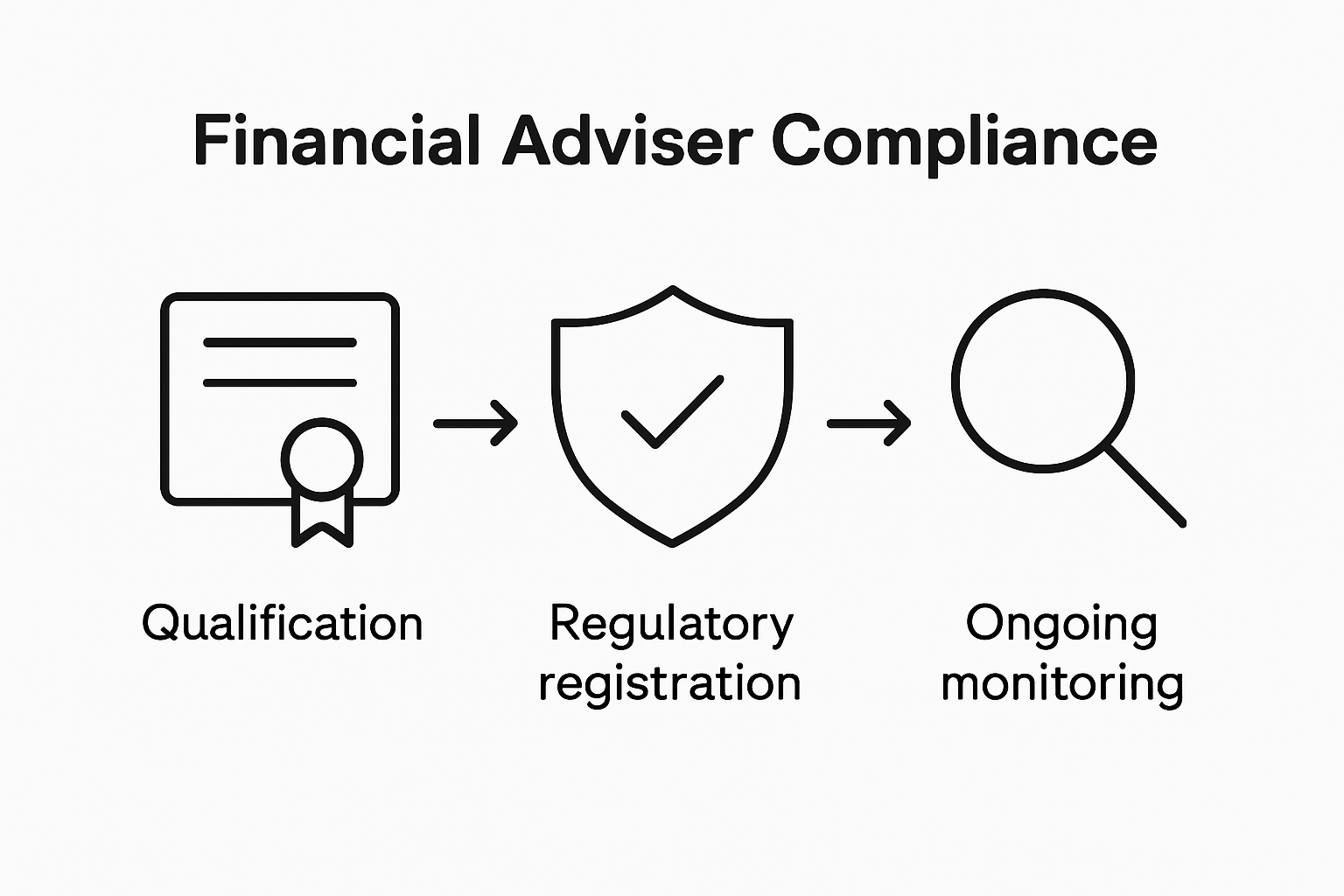

Compliance Requirements for Advisers

Independent financial advisers must navigate complex regulatory landscapes, demonstrating comprehensive professional competence and adherence to stringent industry standards. The compliance journey involves multiple critical stages that ensure financial professionals maintain the highest levels of professional integrity and client protection.

Regulatory requirements vary significantly across different jurisdictions, with each region implementing unique authorisation protocols. For instance, in France, financial advisers must obtain explicit authorisation from the Financial Markets Authority (AMF) and comply with specific regulatory standards that govern their professional conduct and client interactions.

Key compliance requirements typically encompass:

Professional Qualifications

Minimum academic credentials in finance or related disciplines

Mandatory professional certification programmes

Ongoing professional development requirements

Ethical Standards

Comprehensive client needs assessment protocols

Full disclosure of potential conflicts of interest

Transparent fee structure documentation

Regulatory Documentation

Regular submission of professional practice reports

Maintenance of detailed client interaction records

Compliance with data protection and privacy regulations

These multifaceted compliance frameworks serve as crucial safeguards, ensuring that financial advisers operate with transparency, competence, and unwavering commitment to their clients’ financial well-being. By implementing rigorous standards, regulatory bodies create an environment of trust, accountability, and professional excellence that protects investors and maintains the integrity of financial services globally.

Risks of Unregulated Financial Advice

Unregulated financial advice presents significant potential for serious financial misconduct and client exploitation. Principal-agent problems can emerge when financial advisers operate without comprehensive oversight, creating environments where dishonest practices and conflicting interests may proliferate unchecked.

The rapid growth of complex financial markets has amplified concerns about potential systemic risks associated with unregulated financial services. Financial institutions and regulatory bodies increasingly recognise the critical importance of maintaining robust frameworks that prevent potential financial misconduct and protect investor interests.

Potential risks of unregulated financial advice include:

Financial Misrepresentation

Concealment of investment risks

Deliberate misstatement of potential returns

Manipulation of investment recommendations

Conflict of Interest

Recommending products with highest personal commissions

Prioritising personal financial gain over client objectives

Undisclosed financial relationships with product providers

Inadequate Professional Standards

Lack of mandatory qualifications

Absence of ongoing professional development

No mechanism for complaint resolution

These unregulated environments create significant vulnerabilities for investors, particularly those with limited financial literacy or complex investment needs. By operating outside established regulatory frameworks, unqualified advisers can potentially cause substantial financial harm, undermining investor confidence and exposing individuals to unnecessary financial risks.

Secure Your Financial Future with Regulated Experts You Can Trust

Navigating the complex landscape of financial adviser regulatory bodies is essential to avoid the risks of unregulated advice and ensure your investments are managed by professionals who meet stringent qualifications and ethical standards. The article emphasises challenges such as inconsistent international regulations and the dangers of financial misconduct that can arise without proper oversight. If you seek clarity and confidence, it is critical to connect with financial advisers who are verified, regulated, and compliant with local authorities worldwide.

Discover how Linkindependent.com simplifies this crucial process by matching you with verified, fully regulated financial advisers who adhere to rigorous compliance requirements. By using our platform, you benefit from transparent fee structures and personalised recommendations tailored to your unique financial goals. Act now to confidently manage cross-border investments or complex financial planning with experts vetted through global regulatory standards. Start your journey today by visiting Linkindependent.com and take the next step towards secure, trustworthy financial guidance.

Frequently Asked Questions

What are financial adviser regulatory bodies?

Financial adviser regulatory bodies are institutions that set and enforce professional standards for financial advisers. They ensure that advisers are properly trained, licensed, and adhere to ethical guidelines, ultimately protecting investors.

How do financial adviser regulatory bodies protect clients?

These bodies implement oversight measures such as mandatory qualifications, background checks, and stringent complaint resolution processes to safeguard investors from financial misconduct and ensure professional integrity.

What are the key responsibilities of financial adviser regulatory bodies?

Key responsibilities include establishing professional qualification requirements, monitoring the conduct of financial advisers, investigating complaints, and maintaining public records of licensed advisers to enhance transparency and accountability.

What risks are associated with unregulated financial advice?

Unregulated financial advice can lead to financial misrepresentation, conflicts of interest, and inadequate professional standards, posing significant risks to investors, especially those with limited financial knowledge.

Recommended

Comments