Investment risk profiling for cross-border investors

- a few seconds ago

- 9 min read

Many investors mistakenly treat risk profiling as a checkbox exercise completed once and forgotten. In reality, investment risk profiling is a dynamic process that evaluates your tolerance for financial uncertainty, aligns it with your goals, and adapts to changing circumstances. For individuals managing cross-border investments, this process becomes even more critical as currency fluctuations, varying tax regimes, and geopolitical shifts constantly reshape your risk landscape.

Table of Contents

Key takeaways

Point | Details |

Dynamic profiling essential | Risk profiles must evolve with personal circumstances and international market conditions, requiring regular reassessment every 12 to 24 months. |

Cross-border complexity | Currency volatility, taxation differences, and geopolitical events introduce unique risks that traditional profiling often overlooks. |

Behavioural insights improve accuracy | Integrating behavioural finance frameworks can enhance risk prediction accuracy significantly compared to classical questionnaire-based methods. |

Expert guidance matters | Regulated financial advisers provide tailored strategies that account for international complexities and regulatory requirements. |

Introduction to investment risk profiling

Investment risk profiling systematically assesses how much financial uncertainty you can handle whilst pursuing your investment objectives. This process combines three core components: your psychological comfort with volatility (risk tolerance), your financial aspirations (goals), and the timeframe for achieving them (investment horizon). Together, these elements create a personalised blueprint that guides asset allocation decisions and portfolio construction.

For international investors, the profiling process must extend beyond traditional domestic considerations. Cross-border portfolios face amplified volatility from currency movements, divergent regulatory environments, and geopolitical developments that can dramatically alter risk-return calculations. A comprehensive profile accounts for these international dimensions whilst remaining flexible enough to adapt as circumstances change.

Key aspects of effective risk profiling include:

Quantitative assessment of financial capacity to absorb losses

Psychological evaluation of emotional responses to market downturns

Time horizon analysis considering both short-term needs and long-term objectives

International context integration including currency exposure and tax implications

Without proper profiling, you risk building portfolios that either expose you to excessive volatility or fail to generate sufficient returns for your goals. The stakes are even higher when managing assets across multiple jurisdictions, where misjudging risk tolerance can lead to costly tax inefficiencies or regulatory complications.

How risk profiling is quantified and adapted for cross-border investors

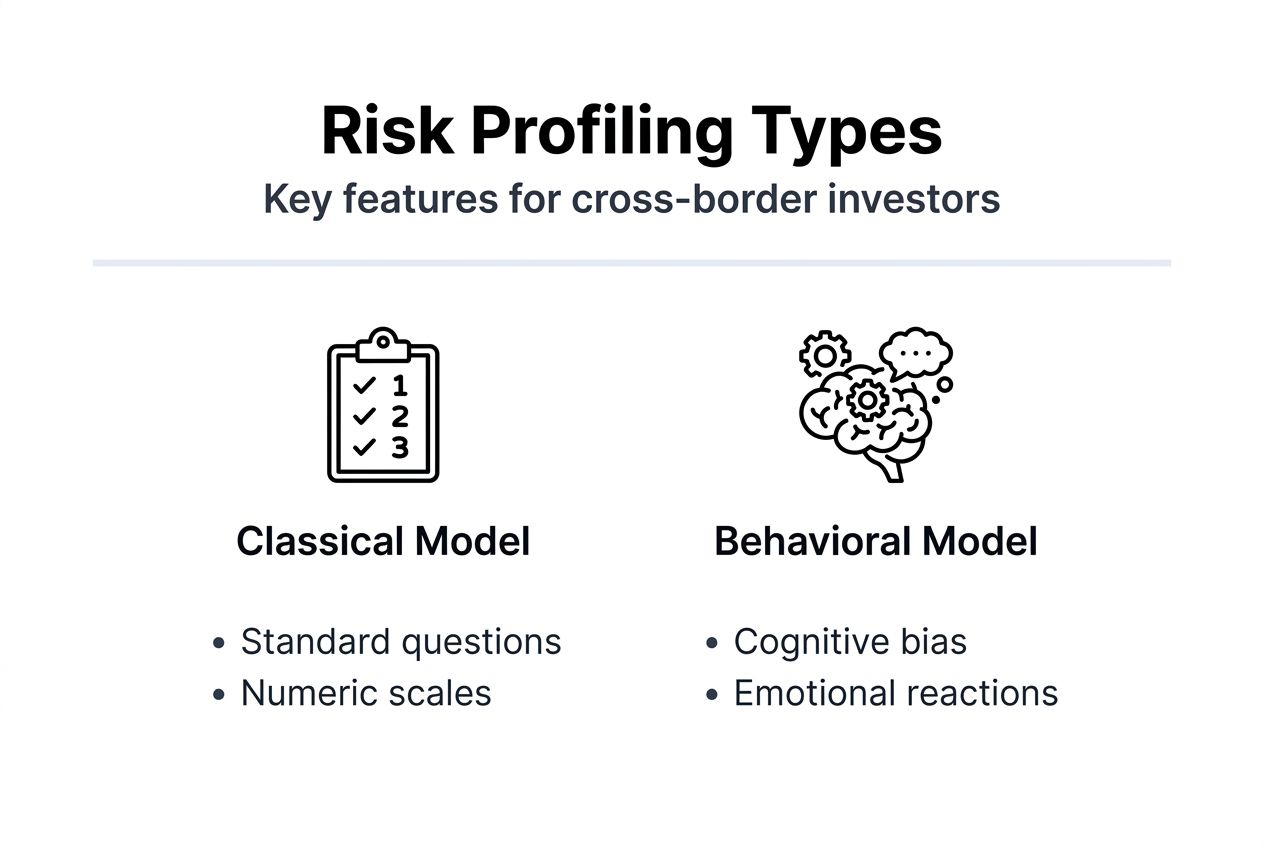

Standardised tools like FinaMetrica provide structured questionnaires that score risk tolerance on numeric scales, creating consistency across different advisers and institutions. These classical approaches typically assess your financial situation, investment experience, and reactions to hypothetical market scenarios. Whilst useful as starting points, they often miss the psychological nuances that drive actual investment behaviour during market stress.

Behavioural finance principles enhance traditional profiling by examining cognitive biases, emotional responses, and decision-making patterns under uncertainty. Research shows behavioural approaches improve risk prediction accuracy by up to 30% compared to questionnaire-only methods. These frameworks recognise that investors often act irrationally during volatility, overweighting recent experiences or panicking during downturns regardless of their stated risk tolerance.

For cross-border investors, cultural context matters significantly. Risk perception varies across cultures, with some societies embracing investment uncertainty whilst others prioritise capital preservation. Your psychological risk tolerance may shift when investing in unfamiliar markets or currencies, requiring advisers to adjust profiling approaches accordingly. Regulated financial advisers worldwide increasingly incorporate these cultural dimensions into their assessment processes.

Adaptations for international investors include:

Currency risk tolerance evaluation separate from market risk assessment

Tax efficiency considerations integrated into risk-return calculations

Geopolitical stability preferences factored into country allocation decisions

Regulatory familiarity levels influencing market selection

Pro Tip: Request a behavioural assessment alongside traditional questionnaires when working with advisers. This dual approach captures both your intellectual understanding of risk and your likely emotional responses during actual market turbulence.

Challenges and additional risks in cross-border investment profiling

Currency volatility introduces a layer of unpredictability absent from domestic portfolios. When your base currency differs from your investment currencies, exchange rate movements can dramatically amplify or diminish returns. Studies indicate currency volatility can add up to 15 to 20% increase in portfolio risk for global investors, yet traditional risk profiles rarely quantify this exposure adequately.

Taxation differences fundamentally alter your effective risk tolerance across jurisdictions. A 10% portfolio decline in a tax-advantaged account impacts you differently than the same loss in a highly taxed environment. Capital gains treatment, dividend taxation, wealth taxes, and estate duty all influence how much risk you can reasonably accept. Cross-border investors must factor in tax treaty provisions and potential double taxation when assessing suitable risk levels.

Geopolitical instability creates risks that resist traditional quantification methods. Regulatory changes, trade disputes, sanctions, and political upheaval can rapidly reshape investment landscapes in ways that correlate poorly with historical data. What appears as moderate risk during stable periods can transform into severe volatility during geopolitical shocks. Your risk profile must acknowledge these tail risks explicitly rather than assuming future stability mirrors past conditions.

Additional complications facing international investors include:

Differing investor protection standards across jurisdictions

Variable liquidity profiles in less developed markets

Information asymmetries when investing in unfamiliar regulatory environments

Repatriation risks in countries with capital controls

Currency movements, taxation variability, and geopolitical uncertainty compound traditional investment risks, requiring cross-border investors to adopt more sophisticated profiling approaches that explicitly account for these international dimensions rather than treating them as afterthoughts.

Common misconceptions about investment risk profiling

Many investors view risk profiling as a one-time exercise completed when opening an account or starting with a new adviser. This static approach ignores how life circumstances, financial situations, and market conditions evolve continuously. Your risk tolerance at 35 with growing income differs markedly from your capacity at 55 approaching retirement, yet portfolios often remain unchanged for years without reassessment.

Confusion between risk tolerance and risk aversion leads to suboptimal portfolio construction. Risk tolerance describes your capacity to withstand losses without jeopardising financial goals. Risk aversion reflects your psychological discomfort with uncertainty. You might have high financial capacity for risk but deep psychological aversion, requiring advisers to balance these competing factors rather than focusing solely on one dimension.

Another frequent mistake involves overlooking tax and geopolitical factors when profiling international portfolios. Domestic risk profiling tools rarely incorporate these elements systematically, leaving cross-border investors with incomplete assessments. For investment suitability for US expats, ignoring tax treaty implications or foreign account reporting requirements can lead to portfolios that appear appropriate on paper but create compliance nightmares in practice.

Common pitfalls include:

Assuming past risk tolerance predicts future behaviour during actual market stress

Neglecting to update profiles after major life events like marriage, children, or career changes

Failing to distinguish between short-term volatility tolerance and long-term loss capacity

Overlooking how home bias distorts international risk perceptions

These misconceptions often result in portfolios misaligned with actual risk capacity, leading either to excessive conservatism that fails to meet goals or dangerous overexposure during market downturns. Regular profiling reviews combined with behavioural insights help avoid these traps.

Comparing risk profiling frameworks for international investors

Classical questionnaire-based models dominate the advisory industry due to their standardisation and regulatory acceptance. These tools typically feature 10 to 25 questions covering financial situation, investment experience, time horizon, and hypothetical scenario responses. Scoring algorithms then categorise you into risk bands like conservative, moderate, or aggressive. Whilst reliable for basic segmentation, they struggle to capture behavioural nuances or international complexity.

Behavioural finance-based frameworks integrate psychological assessments that examine how you actually make decisions under uncertainty. These approaches evaluate cognitive biases like loss aversion, recency bias, and overconfidence through scenario-based questioning and personality assessments. Research demonstrates behavioural approaches improve risk prediction accuracy by up to 30% by capturing emotional factors that traditional questionnaires miss.

Framework aspect | Classical questionnaires | Behavioural approaches |

Assessment method | Standardised questions with numeric scoring | Scenario-based with psychological evaluation |

Accuracy for international context | Moderate, lacks cultural adaptation | Higher, incorporates psychological variability |

Regulatory acceptance | Widely accepted, established track record | Growing acceptance, requires expertise |

Time investment | 15 to 30 minutes | 45 to 90 minutes |

Cost | Lower, often automated | Higher, requires specialist interpretation |

Adaptation frequency | Annual or biennial typically | Quarterly or after significant events |

For international investors, hybrid models combining both approaches offer optimal results. Classical tools provide the standardised baseline required for regulatory compliance, whilst behavioural assessments add depth regarding how you’ll likely respond to currency volatility, geopolitical shocks, or unfamiliar market conditions. This combination creates more resilient profiles that withstand the complexity of cross-border investing.

Pro Tip: Ask potential advisers which profiling framework they use and whether they adapt it for international circumstances. Advisers relying solely on generic questionnaires may lack the sophistication required for complex cross-border portfolios.

Applying investment risk profiling to cross-border portfolio management

Translating risk profiles into practical portfolio strategies requires systematic integration of profiling insights with international investment realities. Effective application follows a structured process:

Map your risk score to asset allocation ranges that account for currency exposure as a distinct risk factor rather than folding it into equity or bond allocations.

Adjust allocation boundaries based on tax efficiency considerations in each jurisdiction where you hold assets or maintain tax residence.

Incorporate geopolitical risk limits by capping exposure to individual countries or regions based on stability assessments and your tolerance for regulatory uncertainty.

Establish rebalancing triggers that account for currency movements separately from underlying asset performance to avoid mistaking exchange rate fluctuations for investment gains or losses.

Schedule formal risk profile reviews every 12 to 24 months or after major life events, ensuring your portfolio evolves alongside changing circumstances.

Document the reasoning behind allocation decisions explicitly, creating an audit trail that helps you resist emotional reactions during market stress.

Regulated financial advisers specialising in cross-border wealth management bring critical expertise to this application process. Their understanding of regulated financial advisers expertise in navigating international tax treaties, reporting requirements, and multi-jurisdictional compliance ensures your portfolio remains both appropriate for your risk profile and optimised for regulatory efficiency.

Dynamic reassessment proves particularly crucial for international investors. Currency relationships, tax treaty provisions, and geopolitical landscapes shift more rapidly than domestic factors. A comprehensive global wealth management guide emphasises quarterly reviews of international exposure even when formal risk profiling occurs less frequently.

Pro Tip: Maintain a simple risk journal noting your emotional responses during market volatility. This personal record provides invaluable insights during formal profile updates, revealing whether your actual behaviour aligns with your stated risk tolerance. You can request personalised financial advice globally to help interpret these patterns.

Conclusion and next steps for effective risk profiling

Investment risk profiling for cross-border portfolios demands more sophistication than domestic investing. Your profile must evolve continuously, incorporating behavioural insights alongside traditional assessments whilst explicitly accounting for currency risk, tax implications, and geopolitical uncertainty. Static, one-time profiling fails to capture the dynamic nature of international investing, where market conditions and personal circumstances shift rapidly.

Customised, culturally aware profiling offers substantial benefits beyond regulatory compliance. It creates portfolios genuinely aligned with your capacity for risk whilst optimising for tax efficiency across jurisdictions. Behavioural frameworks enhance this process by revealing psychological patterns that traditional questionnaires miss, leading to more resilient strategies during market turbulence.

Expert guidance proves invaluable when navigating these complexities. Regulated advisers with international expertise help translate abstract risk scores into concrete portfolio strategies, ensuring your investments reflect both your financial capacity and psychological comfort across multiple markets and currencies.

Get expert financial advice for cross-border investing

Managing international investments requires more than generic risk profiling tools. You need advisers who understand how currency movements, tax treaties, and geopolitical shifts affect your personal risk landscape.

[

Linkindependent.com connects you with regulated financial professionals worldwide who specialise in cross-border wealth management. Our advisers bring deep expertise in international taxation, multi-currency portfolios, and regulatory compliance across jurisdictions. Whether you’re a US citizen relocating to Europe or managing assets across continents, we match you with experts who understand your unique circumstances. Explore honest financial advice online and discover how regulated financial advisers benefits can transform your international investment strategy.

Frequently asked questions

How often should I update my investment risk profile for cross-border investing?

You should reassess your risk profile every 12 to 24 months at minimum, with additional reviews after major life changes like marriage, career shifts, or international relocations. Cross-border investors face more dynamic conditions than domestic portfolios, making regular updates essential for maintaining alignment between risk tolerance and actual portfolio composition.

What factors make risk profiling for cross-border investors different?

Currency volatility introduces significant additional risk beyond traditional market movements, potentially adding 15 to 20% to portfolio volatility. Taxation rules vary dramatically across jurisdictions, affecting your net returns and risk capacity. Geopolitical events create unpredictable disruptions that domestic investors rarely encounter, requiring explicit consideration in your risk assessment.

Can behavioural finance improve risk profiling accuracy?

Behavioural models capture psychological nuances that traditional questionnaires miss, examining how you actually respond to uncertainty rather than how you think you’ll respond. Studies show behavioural approaches improve risk prediction accuracy by up to 30% compared to questionnaire-only methods. These frameworks complement rather than replace traditional tools, creating more comprehensive assessments for complex international portfolios.

Why is ongoing risk profile reassessment important in international investing?

Market conditions, currency relationships, and tax regulations change constantly, particularly across multiple jurisdictions. Your personal circumstances evolve through career changes, family developments, and shifting financial goals. Regular reassessment ensures your portfolio continues matching your actual risk capacity rather than reflecting outdated assumptions from years past.

Recommended