What Is a Regulated Financial Adviser? Complete Overview

- Dec 3, 2025

- 7 min read

Most people are surprised to learn that british financial advisers must follow some of the world’s strictest regulations, creating powerful protections for their clients. In a financial world full of confusing choices and hidden risks, knowing whether your adviser is officially regulated is more than a box to tick. This guide breaks down who counts as a regulated financial adviser, how their role differ from others, and what every british investor should look for before making any financial decision.

Table of Contents

Key Takeaways

Point | Details |

Role of Regulated Financial Advisers | They provide personalised financial guidance and investment strategies under stringent regulatory oversight, ensuring transparency and client interest. |

Types of Financial Advisers | Advisers vary by specialisation, including Registered Investment Advisers, Chartered Financial Planners, and Wealth Managers, each serving distinct client needs. |

Importance of Regulation | Regulation protects consumers by enforcing ethical standards, requiring transparency, and ensuring advisers maintain professional integrity. |

Choosing Wisely | Clients should thoroughly assess advisers based on credentials, fee structures, and their understanding of individual financial goals to mitigate risks. |

Defining Regulated Financial Advisers and Their Role

A regulated financial adviser is a professional who provides personalised financial guidance and investment recommendations under strict legal oversight from recognised financial regulatory bodies. These experts offer comprehensive financial planning services designed to help individuals, businesses, and investors make informed decisions about wealth management, retirement planning, investment strategies, and risk mitigation.

Regulated financial advisers differ from unregulated professionals by maintaining rigorous professional standards and legal accountability. Their core responsibilities involve analysing clients’ financial situations, developing tailored investment strategies, managing portfolios, and providing strategic recommendations aligned with individual financial goals. They are legally required to act in their clients’ best interests, which means offering transparent, unbiased advice that prioritises the client’s financial wellbeing over personal commissions or incentives.

The critical distinguishing feature of regulated financial advisers is their mandatory compliance with governmental and professional regulatory frameworks. This means they must:

Hold appropriate professional qualifications

Maintain professional indemnity insurance

Undergo regular professional competency assessments

Adhere to strict ethical guidelines

Provide transparent fee structures

Maintain comprehensive record-keeping

For international clients with complex financial portfolios, working with a regulated financial adviser becomes even more crucial. These professionals understand cross-border financial regulations, can navigate intricate international investment landscapes, and provide nuanced guidance that takes into account global economic trends and jurisdiction-specific legal requirements.

Types of Financial Advisers and Key Distinctions

Financial advisers are not a monolithic group, but rather a diverse profession with multiple specialisations tailored to different client needs and financial objectives. Certified Financial Planners (CFPs) represent one of the most comprehensive professional categories, offering holistic financial guidance that encompasses retirement planning, investment strategies, tax management, and comprehensive wealth preservation techniques.

Wealth managers and portfolio managers represent another critical segment of financial advisory services, each with distinct areas of expertise. Wealth managers typically work with high-net-worth individuals, providing intricate financial planning that goes beyond basic investment advice. They develop sophisticated strategies addressing complex financial scenarios, including estate planning, tax optimisation, and intergenerational wealth transfer. Portfolio managers, by contrast, focus more narrowly on investment selection, asset allocation, and ongoing portfolio performance monitoring.

The primary categories of financial advisers can be distinguished by their specific qualifications and service offerings:

Registered Investment Advisers (RIAs): Legally registered professionals who provide detailed investment management services

Chartered Financial Consultants (ChFCs): Specialists with advanced training in comprehensive financial planning

Insurance-based Financial Advisers: Professionals focusing on risk management and protection strategies

Independent Financial Advisers: Unaffiliated professionals offering unbiased recommendations across multiple financial products

For international clients with complex cross-border financial interests, selecting the right type of financial adviser becomes paramount. These professionals must not only understand diverse investment landscapes but also navigate intricate regulatory environments, tax implications, and global economic dynamics. The most effective advisers combine deep technical expertise with a nuanced understanding of individual client circumstances, ensuring personalised financial strategies that adapt to changing economic conditions and personal life stages.

Qualifications, Licensing, and Regulatory Authorities

Financial advisers must navigate a complex landscape of professional qualifications and regulatory requirements to legally provide financial guidance. The journey to becoming a fully licensed financial adviser involves rigorous educational standards, comprehensive examinations, and ongoing professional development that ensures practitioners maintain the highest levels of competence and ethical conduct.

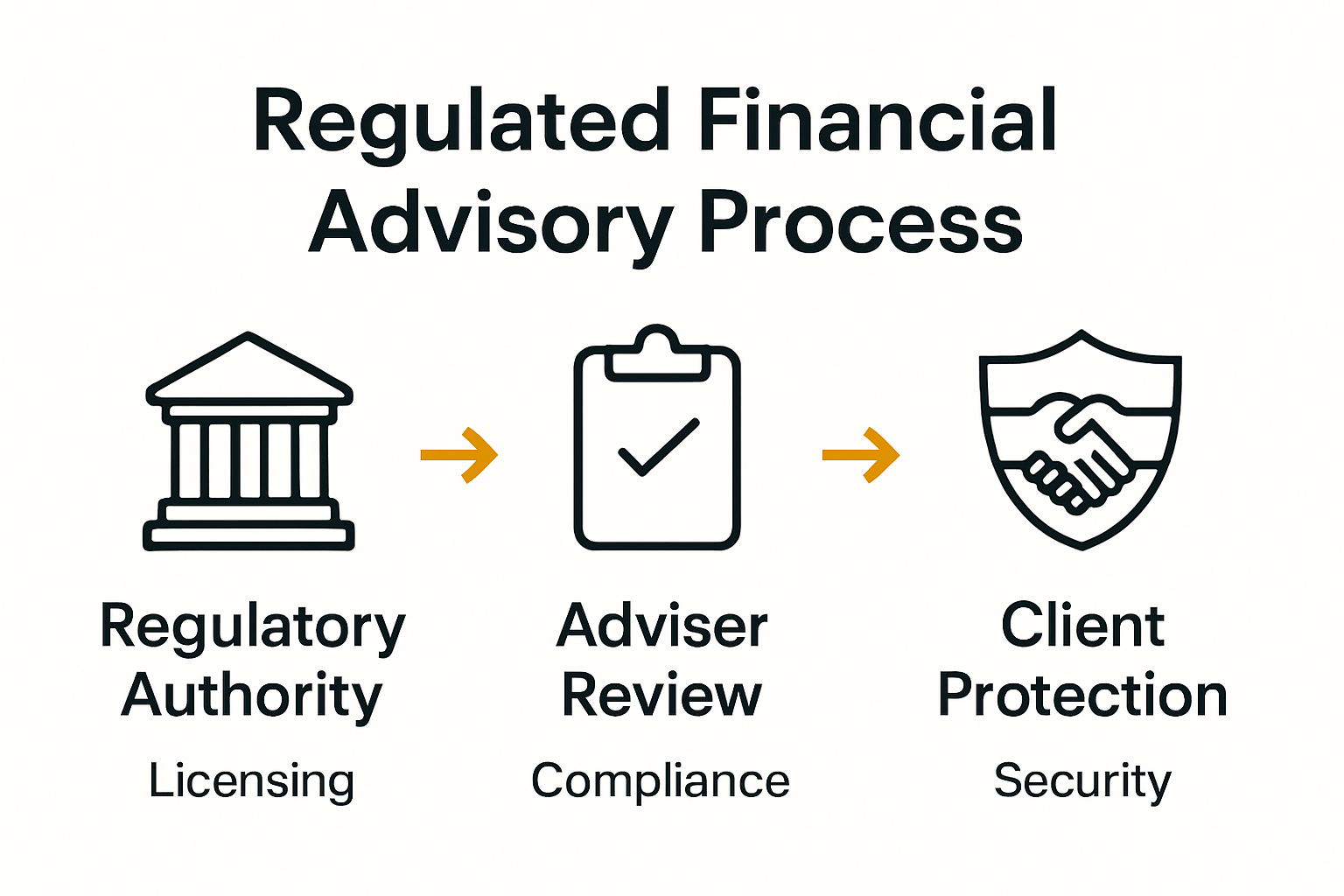

The licensing process is meticulously designed to protect client interests and maintain professional integrity. Regulatory authorities play a crucial role in overseeing financial advisers, with bodies like the Financial Conduct Authority (FCA) establishing stringent guidelines for professional practice. These regulatory frameworks mandate specific licensing requirements that financial advisers must meet and continuously uphold, including:

Completion of recognised professional qualifications

Passing comprehensive professional competency examinations

Maintaining mandatory professional indemnity insurance

Undergoing regular compliance and competency assessments

Adhering to strict ethical and professional conduct standards

Professional certifications represent a critical component of a financial adviser’s credentials. The most respected qualifications include Chartered Financial Analyst (CFA), Certified Financial Planner (CFP), and Chartered Financial Consultant (ChFC) designations. Each certification requires extensive study, practical experience, and a commitment to ongoing professional development, ensuring that advisers remain at the forefront of financial expertise and regulatory compliance.

For international clients, understanding the nuanced regulatory landscape becomes paramount. Different jurisdictions maintain varying standards for financial advisory qualifications, creating a complex environment where cross-border financial advice requires exceptional expertise. The most accomplished financial advisers demonstrate not just technical proficiency, but also a deep understanding of global regulatory frameworks, ensuring clients receive guidance that is both legally compliant and strategically sophisticated.

Why Regulation Matters: Protection and Transparency

Financial regulation represents a critical safeguard that protects consumers from potential misconduct and ensures the integrity of financial advisory services. By establishing comprehensive frameworks that mandate transparency, accountability, and ethical conduct, regulatory bodies create a robust protective environment that shields clients from unscrupulous practices and potential financial exploitation.

The mechanisms of financial regulation extend far beyond simple oversight, creating intricate systems designed to maintain professional standards and client confidence. Consumer protection becomes the cornerstone of these regulatory frameworks, with key protective measures including:

Mandatory disclosure of potential conflicts of interest

Rigorous background checks for financial professionals

Comprehensive complaint and dispute resolution processes

Strict requirements for maintaining accurate financial records

Enforced professional liability and indemnity insurance

Transparency emerges as a fundamental principle in regulated financial advisory services. Regulated advisers must provide clear, comprehensible documentation about their fee structures, investment recommendations, and potential risks. This approach ensures clients can make informed decisions, understanding exactly what services they are receiving and the potential implications of their financial strategies.

For international clients navigating complex financial landscapes, regulation provides an additional layer of security. The most sophisticated regulatory frameworks create cross-jurisdictional standards that protect clients’ interests, regardless of geographical boundaries. By mandating consistent professional conduct, comprehensive risk assessment, and client-centric approaches, these regulations transform financial advice from a potentially risky transaction into a structured, trustworthy professional service.

Risks, Costs, and How to Choose Wisely

Selecting a financial adviser involves carefully navigating potential risks and understanding complex fee structures that can significantly impact your financial outcomes. The financial advisory landscape is fraught with potential pitfalls, ranging from hidden charges to misaligned investment strategies that could compromise your long-term financial objectives.

Different financial advisers employ varied fee models, each with unique implications for clients’ investment portfolios. The primary fee structures include:

Percentage-based fees: Typically 0.5% to 1.5% of assets under management annually

Flat fee arrangements: Fixed annual or hourly rates for specific services

Commission-based compensation: Payment derived from financial product sales

Hybrid models: Combining multiple fee approaches

When evaluating potential financial advisers, prudent clients should conduct thorough due diligence. Critical assessment criteria include verifying professional credentials, examining track records, understanding complete fee structures, and assessing alignment with personal financial goals. Requesting comprehensive disclosure documents, checking regulatory records, and conducting initial consultation interviews can provide crucial insights into an adviser’s competence and integrity.

For international clients with complex financial portfolios, choosing a financial adviser becomes an even more nuanced process. The ideal adviser must demonstrate not just technical expertise, but also a sophisticated understanding of cross-border financial regulations, tax implications, and global investment strategies. Success hinges on finding a professional who can offer personalised guidance that transcends geographical boundaries while maintaining the highest standards of transparency and client-centric service.

Find Your Trusted Regulated Financial Adviser Today

Understanding the complexities of regulated financial advisers can feel overwhelming, especially when you face the challenge of navigating different regulations, fee structures, and professional qualifications. This article highlights the importance of working with licensed and accountable professionals who prioritise your financial wellbeing without hidden conflicts or unclear fees. Whether you need guidance on international investments, wealth management, or tax optimisation, trust is essential to avoid costly mistakes and ensure transparent, personalised advice.

Don’t leave your financial future to chance. At Link Independent we specialise in connecting you with verified, regulated financial advisers who meet the highest professional and regulatory standards such as FCA, SEC, and ESMA. Access tailored consultations with experts who understand cross-border complexities and provide clear fee structures that protect your interests. Visit Link Independent now to begin your search for a dependable financial professional who can guide you with confidence and clarity.

Frequently Asked Questions

What is a regulated financial adviser?

A regulated financial adviser is a professional who provides tailored financial guidance and investment advice under strict legal oversight from recognised regulatory bodies. They prioritise clients’ interests and must adhere to professional standards and ethical guidelines.

Why is it important to work with a regulated financial adviser?

Working with a regulated financial adviser ensures that you receive trustworthy and transparent financial advice. These professionals are legally obligated to act in your best interests, providing an added layer of protection against potential misconduct and ensuring compliance with ethical standards.

What qualifications should I look for in a financial adviser?

Key qualifications to look for include professional designations such as Chartered Financial Analyst (CFA), Certified Financial Planner (CFP), and Chartered Financial Consultant (ChFC). Additionally, advisers should be compliant with licensing requirements set by regulatory authorities and possess ongoing professional development.

How do financial advisers charge for their services?

Financial advisers can charge in various ways, including percentage-based fees (usually a percentage of assets under management), flat fees for specific services, commission-based compensation from financial products, or hybrid models that combine these approaches.

Recommended

Comments