Financial Regulation – Why It Matters for US Expats

- Jan 17

- 7 min read

Moving from the United States to Europe often means facing a maze of new financial rules and planning decisions. For many American expats, understanding how financial regulation shapes tax management and investment planning is more than a formality—it is the key to protecting savings and avoiding unexpected hurdles. By exploring how financial regulation operates across borders, this guide offers practical insight for anyone aiming to safeguard their interests and stay compliant in a new European environment.

Table of Contents

Key Takeaways

Point | Details |

Understanding Financial Regulation | Financial regulation ensures stability and fairness in financial systems, protecting consumers and maintaining economic integrity. |

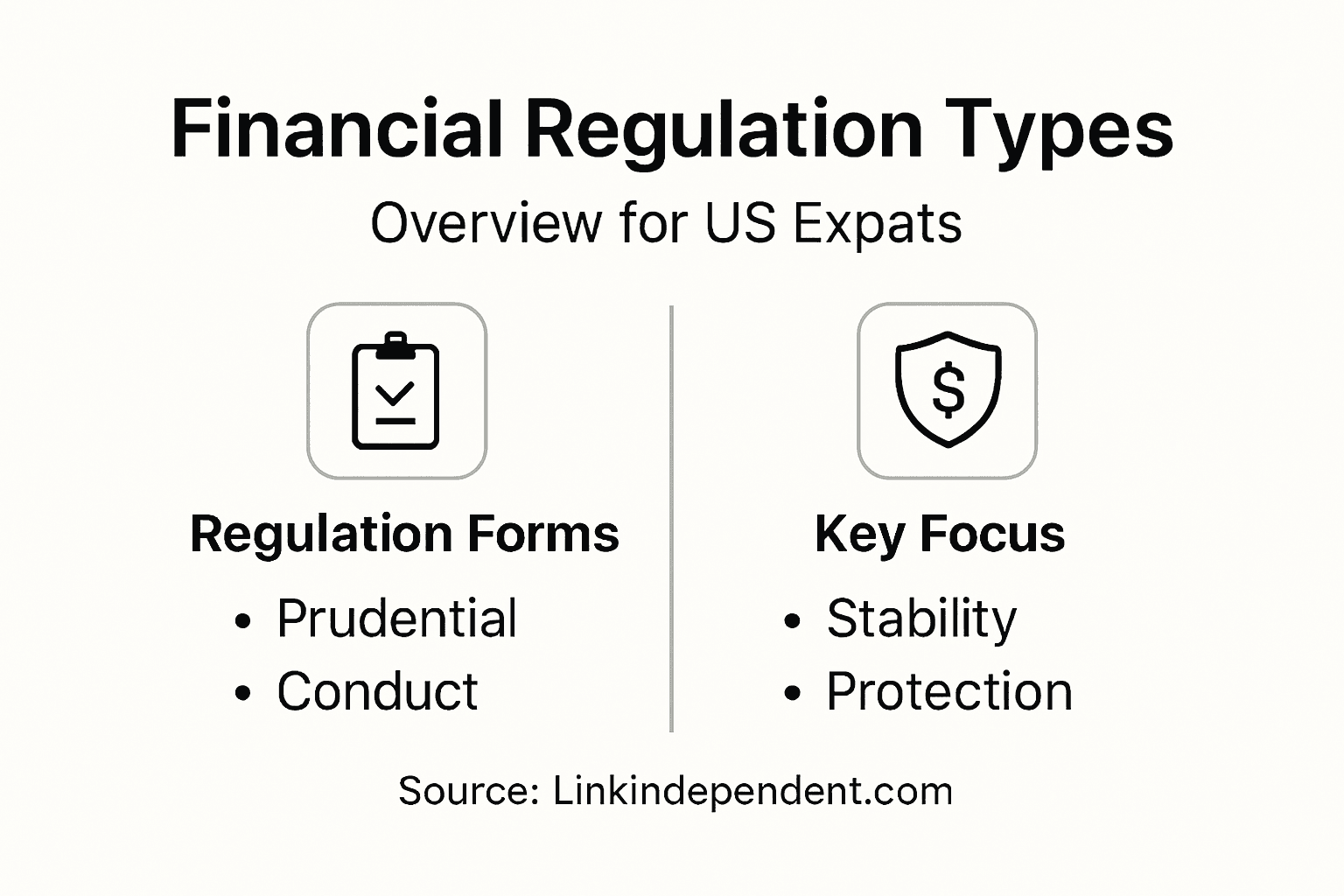

Types of Regulation | Key categories include prudential regulation, conduct regulation, and market regulation, each serving to protect investor interests and ensure system stability. |

Cross-Border Compliance | Financial advisers must navigate diverse jurisdictional regulations, including licensing and anti-money laundering standards, to operate internationally. |

Managing Compliance Risks | Proactive compliance strategies, including working with specialised advisers and employing digital tracking tools, are essential for US expats to mitigate regulatory risks. |

Defining Financial Regulation and Its Purpose

Financial regulation represents a structured framework designed to maintain stability, transparency, and fairness within financial systems. At its core, this system governs how financial institutions operate, ensuring they protect consumers, maintain economic integrity, and minimise systemic risks. Financial regulators create comprehensive rules and guidelines that financial service providers must follow to prevent misconduct and protect individual investors.

The primary objectives of financial regulation extend far beyond simple oversight. Economic reasons for regulatory intervention stem from addressing inherent market failures that could potentially harm investors and destabilise economic structures. Key goals include protecting investors, maintaining financial system stability, preventing financial crimes, and ensuring market efficiency. Regulators achieve these objectives through strategic approaches such as establishing entry requirements, monitoring institutional conduct, mandating transparent information disclosure, and enforcing prudential standards.

For US expats navigating international financial landscapes, understanding these regulatory frameworks becomes critically important. Different countries implement varied regulatory mechanisms, which can significantly impact investment strategies, tax obligations, and financial planning. Some fundamental regulatory mechanisms include licensing requirements for financial advisers, mandatory reporting standards, capital adequacy rules, and consumer protection protocols. These frameworks help ensure that financial service providers operate with integrity and accountability, ultimately safeguarding individual investors’ interests.

Pro tip: Always verify a financial adviser’s regulatory credentials and registration status before engaging their services, especially when operating across international boundaries.

Types of Financial Regulation Worldwide

Financial regulation is not a monolithic system but a diverse framework comprising multiple approaches tailored to different economic contexts and jurisdictional requirements. Financial market regulations typically fall into three primary categories: prudential regulation, conduct regulation, and market regulation. Each type serves a distinct purpose in maintaining financial system integrity and protecting investor interests.

Prudential Regulation focuses on the financial health and stability of institutions. This approach involves setting capital requirements, monitoring risk management practices, and ensuring banks and financial organisations maintain sufficient reserves to withstand potential economic shocks. Regulators establish stringent guidelines about how much capital institutions must hold, their investment strategies, and their ability to manage potential financial risks.

Conduct regulation and market regulation complement prudential frameworks by addressing consumer protection and market efficiency. Conduct Regulation specifically targets the behaviour of financial service providers, mandating fair treatment of customers, transparent pricing, and clear disclosure of financial products’ risks and terms. Market regulation, meanwhile, concentrates on maintaining overall market integrity, preventing market manipulation, and ensuring fair trading practices. These regulatory mechanisms are particularly crucial for US expats navigating complex international financial environments, where regulatory standards can vary significantly between jurisdictions.

Pro tip: Research the specific regulatory frameworks of your destination country and consult with cross-border financial specialists to understand nuanced compliance requirements.

Legal Frameworks in Europe and USA

Comparative financial regulation approaches reveal fascinating differences between European and United States regulatory systems. While both regions aim to protect financial markets and investors, their legal frameworks reflect distinct philosophical and structural approaches to financial governance. The fundamental variations stem from historical legal traditions, economic priorities, and institutional structures that shape how financial regulations are conceived and implemented.

In the European context, regulatory frameworks tend to emphasise a principles-based approach, which provides broader guidelines allowing more interpretative flexibility. European regulators focus on overarching objectives, enabling financial institutions to adapt implementation strategies while maintaining core regulatory intentions. By contrast, the United States typically employs a more prescriptive regulatory model, characterised by detailed, specific rules that financial institutions must follow precisely. This approach creates a more structured environment with clearer, more explicit compliance requirements.

Here’s a comparison of financial regulation frameworks in Europe and the USA:

Aspect | Europe (Principles-Based) | USA (Prescriptive) |

Regulatory Approach | Flexible, guideline-based | Strict, rule-based |

Main Regulatory Bodies | ECB, ESMA | SEC, Federal Reserve |

Compliance Flexibility | High – interpretation allowed | Low – strict adherence needed |

Typical Documentation | Policy statements, strategic plans | Detailed records, formal forms |

Key regulatory bodies play critical roles in both regions. In the European Union, institutions like the European Central Bank and European Securities and Markets Authority coordinate cross-border financial regulations. The United States relies on agencies such as the Securities and Exchange Commission (SEC) and the Federal Reserve to manage financial oversight. These differences reflect broader systemic approaches to risk management, market efficiency, and investor protection. For US expats navigating international financial landscapes, understanding these nuanced regulatory distinctions becomes essential for making informed financial decisions and ensuring compliance across jurisdictions.

Pro tip: When operating across international financial systems, consult specialists who understand both European and American regulatory frameworks to navigate potential compliance complexities.

Obligations for Cross-Border Financial Advisers

Cross-border compliance challenges represent a complex landscape for financial professionals operating internationally. Financial advisers must navigate intricate regulatory requirements that extend far beyond traditional domestic advisory frameworks. The fundamental challenge lies in understanding and adhering to multiple jurisdictional regulations simultaneously, each with its unique set of legal and compliance expectations.

Licensing Requirements form the cornerstone of cross-border financial advisory obligations. Advisers must secure appropriate authorisations in each jurisdiction where they provide financial services, which often involves demonstrating professional qualifications, passing regulatory examinations, and maintaining ongoing professional credentials. This process typically requires comprehensive documentation proving professional competence, financial integrity, and adherence to local regulatory standards. Some jurisdictions may require separate licensing for different financial service categories, adding layers of complexity to international practice.

Beyond licensing, cross-border financial advisers must maintain rigorous compliance with international standards. These include stringent anti-money laundering protocols, data protection regulations, and transparent reporting mechanisms. Advisers must implement robust record-keeping systems that meet the regulatory requirements of multiple jurisdictions, ensure client confidentiality, and provide accurate financial reporting. The European Securities and Markets Authority provides extensive guidance on managing these multifaceted compliance challenges, emphasising the importance of understanding both home and host country regulatory environments.

Below is a summary of key compliance obligations for cross-border financial advisers:

Obligation | Why It Matters | Typical Requirements |

Licensing | Legal authority to advise clients | Examination, credentials review |

Anti-Money Laundering | Prevent financial crimes | Verification procedures |

Data Protection | Safeguard client confidentiality | Secure storage, privacy audits |

Transparent Reporting | Meet jurisdictional standards | Timely and accurate disclosures |

Pro tip: Develop a comprehensive compliance checklist specific to each jurisdiction and invest in ongoing professional training to stay current with evolving international regulatory requirements.

Key Risks, Pitfalls, and How to Stay Compliant

Financial compliance challenges represent a complex landscape for US expats navigating international financial regulations. These challenges extend beyond simple paperwork, encompassing intricate legal, operational, and strategic considerations that can significantly impact financial planning and investment strategies. Understanding these risks is fundamental to maintaining financial integrity and avoiding potential legal and financial complications.

The primary risks for US expats include regulatory non-compliance, which can result in substantial financial penalties, potential legal proceedings, and reputational damage. Common pitfalls involve misunderstanding local reporting requirements, failing to declare international assets correctly, and inadvertently violating tax treaties between jurisdictions. US citizens must be particularly vigilant about Foreign Account Tax Compliance Act (FATCA) requirements, which mandate detailed reporting of foreign financial assets and accounts. Navigating these complex regulations often requires specialised knowledge and continuous monitoring of changing international financial standards.

To effectively manage these risks, US expats should adopt a proactive compliance strategy. This involves working with qualified cross-border financial advisers who understand both US and local jurisdictional requirements, maintaining meticulous financial records, and implementing robust compliance tracking systems. Regular professional consultations, staying informed about regulatory changes, and leveraging technological solutions for compliance management can significantly mitigate potential risks. Understanding the nuanced differences in financial regulations across jurisdictions is not just a legal necessity but a critical component of successful international financial planning.

Pro tip: Invest in professional compliance consultation and utilise digital tracking tools to maintain accurate and up-to-date international financial reporting.

Navigate Complex Financial Regulations with Confidence

Understanding financial regulation is vital for US Expats managing cross-border finances and investments. The challenges of navigating diverse international frameworks, adhering to licensing and compliance obligations, and avoiding costly pitfalls demand expert guidance. Whether dealing with prudential requirements, anti-money laundering protocols, or tax declarations such as FATCA, securing advice from verified, regulated professionals is essential to protect your assets and maintain financial stability.

At Linkindependent.com, we simplify your search for trusted cross-border financial advisers who are fully compliant with both US and local regulations. Our platform connects you directly to experts specialising in wealth planning, international taxation, and pension management, ensuring you receive personalised support tailored to your unique situation. Act now to navigate these complex regulatory landscapes smoothly and safeguard your financial future.

Find the right financial guidance today by starting with our easy three-step process at Linkindependent.com. Explore how our verified network of international professionals can help you comply confidently, optimise your investments, and secure your financial wellbeing no matter where you are based.

Frequently Asked Questions

What is the purpose of financial regulation for US expats?

Financial regulation aims to maintain stability, transparency, and fairness in financial systems. For US expats, understanding these regulations is crucial as they navigate international financial landscapes that affect investment strategies and tax obligations.

What types of financial regulation should US expats be aware of?

US expats should be aware of three primary types of financial regulation: prudential regulation, which focuses on the financial health of institutions; conduct regulation, which ensures fair treatment and transparency; and market regulation, which maintains overall market integrity and prevents manipulation.

How do financial regulations differ between Europe and the USA?

Financial regulations in Europe typically follow a principles-based approach, offering flexibility for institutions, while the USA employs a more prescriptive regulatory model, requiring strict adherence to detailed rules. Understanding these differences is essential for compliance when operating in different jurisdictions.

What are the compliance obligations for cross-border financial advisers?

Cross-border financial advisers must meet various compliance obligations, including obtaining appropriate licensing, adhering to anti-money laundering protocols, ensuring data protection, and maintaining transparent reporting. These obligations vary by jurisdiction and are crucial for legal operation in multiple regions.

Recommended

Comments