Estate planning explained: A US expat's guide for Europe

- 13 minutes ago

- 9 min read

TL;DR:

US expats in Europe face complex cross-border estate and inheritance tax challenges that can lead to double taxation and legal conflicts. Proper planning involves coordinated wills, understanding local laws like forced heirship, and expert advice from professionals knowledgeable in both US and European systems. Early action and thorough documentation are essential to protect family legacies and optimize tax outcomes.

Many US expats living in Europe carry a quiet confidence that their American will covers everything. It almost never does. US expats face both US federal estate tax and local inheritance taxes in Europe, creating a layered tax exposure that catches even financially savvy families off guard. The stakes are significant. Without proper cross-border planning, your estate could face double taxation, legal disputes, and outcomes that directly contradict your wishes. This guide breaks down what you genuinely need to know about estate planning as a US citizen in Europe, from the tax mechanics to the legal traps, and what you can do about it now.

Table of Contents

Key Takeaways

Point | Details |

Double taxation risk | US expats can face estate taxes both in the US and their European country of residence on the same assets. |

Forced heirship challenges | Local laws in countries like France or Spain can override your US will and force asset allocation to family. |

Tailored planning required | Cookie-cutter US estate tools rarely work abroad—work with cross-border experts for effective planning. |

Dual wills advantage | Having a US and local will, carefully coordinated, often avoids costly legal and tax complications. |

What is estate planning and why does it matter abroad?

Estate planning is the process of organising your assets, legal documents, and financial intentions so that your wealth passes to the right people, in the right way, with the least possible tax burden. For most Americans, it conjures images of a will and perhaps a trust. But it is far broader than that.

A solid estate plan includes wills, trusts, power of attorney, beneficiary designations on retirement accounts and life insurance, and a clear analysis of how assets are held across borders. When you move to Europe, every single one of those elements becomes more complicated.

“Estate planning for US expats is not just about writing a will. It is about understanding which country’s laws govern which assets, and engineering your affairs so that both systems work in your favour rather than against you.”

Here is why residency in Europe changes everything:

Your European country of residence may claim the right to tax your worldwide estate, not just assets held locally.

Local succession laws may override your US will in ways you would never anticipate.

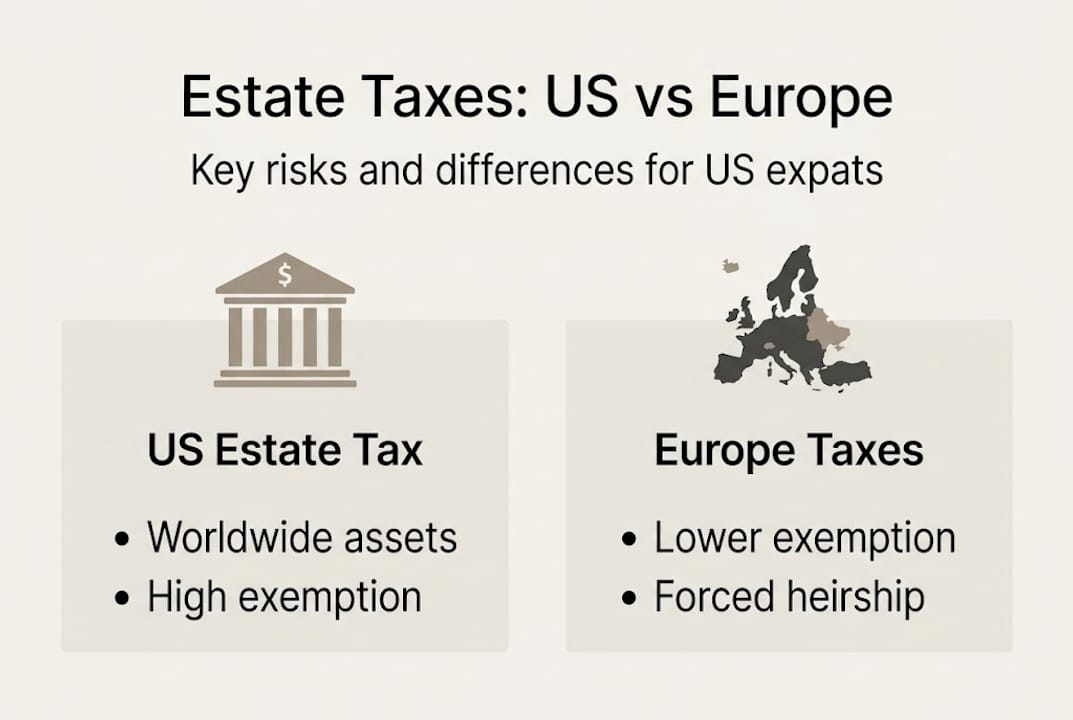

The US federal estate tax applies to worldwide assets for US citizens, with a $15 million exemption in 2026, but European thresholds are often far lower.

Trusts and account structures that work seamlessly in the US may be treated as taxable entities or outright ignored under European law.

Many expats rely on their US-based attorney’s advice without realising that attorney may have little or no knowledge of their host country’s legal system. Reviewing your international estate planning position before or shortly after your move is not optional. It is essential. The cost of getting it wrong is measured not just in money but in family conflict and lost legacies. Exploring wealth planning for US expats is one of the most valuable steps you can take early in your life abroad.

Understanding US and European estate and inheritance taxes

The US taxes its citizens on their worldwide estate regardless of where they live. That is the starting point. But once you add a European country into the picture, you are potentially dealing with two separate tax systems, each with its own rules, thresholds, and rates.

European countries often impose inheritance or estate taxes with lower exemptions and higher rates than the US federal system. In some countries, the tax is levied on the beneficiary rather than the estate itself, which changes the planning approach entirely.

Here is a simplified comparison of how key European countries treat inheritance:

Country | Tax type | Top rate | Key threshold |

France | Inheritance tax | Up to 60% | Varies by relationship |

Germany | Inheritance tax | Up to 50% | €500,000 for spouses |

Belgium | Inheritance tax | Up to 80% | Very low for distant heirs |

Spain | Inheritance tax | Up to 34% | Varies by region |

UK | Estate tax | 40% | £325,000 nil-rate band |

Dual taxation is a genuine risk. Only about 0.1% of US estates pay federal estate tax, but state and European taxes are far more common and punitive, meaning the practical burden for expats often comes from the European side.

Some countries have tax treaties with the US that provide credits or exemptions to prevent full double taxation. However, these treaties have gaps. France, for example, has a treaty with the US, but it does not cover all asset types or all beneficiaries. Germany’s treaty similarly leaves certain situations exposed.

Pro Tip: Do not assume a tax treaty fully protects you. Ask your adviser to map out exactly which assets are covered, which beneficiaries benefit, and where the gaps remain. This analysis alone can reveal significant planning opportunities.

Here is a practical checklist for understanding your cross-border tax exposure:

Identify all assets by country of location and type.

Determine your domicile status in both the US and your European country.

Review any applicable tax treaty between the US and your host country.

Calculate potential estate tax liability under both systems.

Identify credits available to offset double taxation.

For a deeper look at protecting wealth for US expats and understanding cross-border tax planning, specialist guidance is the clearest path forward.

Common traps: Forced heirship, conflicting laws, and misunderstood accounts

Beyond the headline tax numbers, there are legal and structural traps that US expats consistently underestimate. These are the issues that tend to surface only after a death, when it is far too late to fix them.

Forced heirship is one of the most significant. In many civil law countries across Europe, including France, Italy, and Spain, the law mandates that a fixed share of your estate passes to your children or spouse, regardless of what your will says. Forced heirship can override US wills, and while the EU Succession Regulation allows you to elect the law of your nationality to govern your estate, this election is not a complete solution in every situation.

Here is a summary of common traps and their impact:

Trap | Risk level | Who is most affected |

Forced heirship | High | Expats with children or blended families |

US revocable trusts | High | Expats in France, Germany, and Belgium |

Non-US spouse | High | Couples relying on marital deduction |

Foreign retirement accounts | Medium | Expats with 401(k)s and IRAs |

Joint asset titling | Medium | Married couples with mixed assets |

US-style revocable living trusts, a cornerstone of American estate planning, can cause serious problems in Europe. Several European countries do not recognise them or treat the trust assets as directly owned by the settlor, triggering local inheritance tax as if no trust existed at all.

Retirement accounts present another hidden risk. Your 401(k) or IRA may not be treated as a pension under European law. Some countries tax distributions differently or include the account value in the local estate calculation.

Pro Tip: If you are married to a non-US citizen, be aware that the unlimited marital deduction available to US citizen spouses does not apply in the same way. The annual gift exclusion to a non-citizen spouse is capped, and estate planning for mixed-nationality couples requires specific strategies.

Key areas to review immediately after moving:

Beneficiary designations on all retirement accounts and life insurance policies.

How your property is titled, jointly or individually.

Whether your existing trust is recognised under local law.

The impact of your host country’s forced heirship rules on your current will.

For practical international tax tips for expats and expat wealth management strategies, working with advisers who know both systems is not a luxury. It is a necessity.

Best practices: How US expats can successfully plan their estates

The good news is that with the right approach, most of these risks are manageable. The key is acting early and engaging the right expertise. Here is a practical framework to get you started.

Consider pre-move gifting. Gifting assets before you move can reduce both your US and foreign estate liabilities. Annual exclusion gifts and larger lifetime gifts made before establishing European residency may fall outside the scope of your host country’s tax net.

Prepare coordinated dual wills. In many cases, having one will for your US assets and a separate will for your European assets, drafted in the local language and compliant with local law, is the most effective approach. These must be carefully coordinated to avoid one revoking the other.

Review all beneficiary designations. After your move, update the beneficiary designations on your retirement accounts, life insurance, and any payable-on-death accounts to reflect your current wishes and the tax implications in your new country.

Analyse applicable tax treaties. Work with advisers who can identify exactly where treaty protections apply and where they do not, then structure your estate to take full advantage of available credits.

Engage cross-border specialists. Maximising preservation requires using pre-move gifting, dual wills, treaty analysis, and cross-border advice from professionals who operate in both jurisdictions.

Pro Tip: Document every gift, trust amendment, and account change thoroughly. Clear records protect your heirs from disputes and reduce the risk of penalties from either tax authority.

Additional steps worth taking:

Review your power of attorney to ensure it is valid and enforceable in your European country.

Consider whether a local European trust or foundation structure might offer better protection than a US trust.

Reassess your plan every two to three years or whenever your circumstances change significantly.

Seeking multi-jurisdictional advice is the single most effective step you can take to protect your estate across borders.

Why most US expats get estate planning wrong—and how to fix it

Here is the uncomfortable truth: most US expats do not get estate planning wrong because they are careless. They get it wrong because they trust the wrong people. A highly competent US attorney who has never worked with European law, a financial adviser who knows the American system inside out but has never considered French succession rules, these professionals mean well, but their advice is incomplete.

The ‘one-size-fits-all’ US plan is the most common and costly mistake we see. Families discover after a loss that their carefully prepared US trust is ignored by a French court, or that a Belgian inheritance tax bill arrives that nobody anticipated. The grief of losing a loved one is compounded by avoidable financial and legal chaos.

The only reliable solution is proactively coordinated, jurisdiction-aware advice. That means specialists in both the US and European systems working together, not separately. It means reviewing estate planning for expats before you move, or as soon as possible after. Being proactive does not just save money. It protects your family and your legacy.

Next steps: Expert advice for secure cross-border planning

Estate planning as a US expat in Europe is never a simple, standard exercise. Every family’s situation is different, every country has its own rules, and the interaction between US and European law creates complexity that demands genuine expertise.

[

At Linkindependent.com, we connect you with verified, regulated financial advisers, tax professionals, and legal experts who specialise in exactly this kind of cross-border planning. Our matching process takes the guesswork out of finding the right professional for your specific situation. Whether you are planning a move, already living in Europe, or reviewing an existing plan, we can connect you with trusted specialists who understand both sides of the Atlantic. Start your free consultation today and take the first step towards a secure, well-structured estate plan.

Frequently asked questions

Do US expats in Europe still pay US estate tax?

Yes, US expats are subject to US estate tax on worldwide assets regardless of residency, with a $15 million exemption in 2026. Living abroad does not remove this obligation.

What European countries tax US expats’ inheritances the most?

France, Germany, and Belgium impose some of the highest rates, with Belgian inheritance tax reaching 80% for distant heirs and France up to 60%. Europe has 24 of 35 countries with estate or inheritance taxes, making cross-border planning essential.

How do forced heirship laws impact US expats’ wishes?

Forced heirship overrides US wills in civil law countries like France, Italy, and Spain, mandating fixed shares to children or spouses regardless of your stated intentions.

Are dual wills advisable for US expats with European assets?

Often, dual wills coordinated by cross-border advisers work best, with one covering US assets and one covering European assets, carefully drafted to avoid one inadvertently revoking the other.

Recommended

Comments